Jefferies Bumps Up Against Big Rivals as It Looks to Expand - WSJ

Benjamin Lorello, Jefferies LLC’s investment-banking chief, spent years cultivating his relationship with executives at Sirona Dental Systems Inc., helping the small-but-promising health-care company raise money and providing advice on acquisitions. But when Sirona sought an investment bank to lead a $235 million secondary stock offering in 2011, it chose Barclays PLC, because it made “an aggressive offer” to back the entire deal, said Jeffrey Slovin, Sirona’s chief executive. Sirona also selected Barclays to lead a bigger secondary offering of $542 million later that year.

As Jefferies evolves from its roots as a trading firm to a midtier investment bank, it is knocking up against far larger financial firms vying for business, often from companies Jefferies helped to expand. Jefferies has often worked with smaller firms on transactions that bigger rivals may not pursue. As these customers get larger, the competition intensifies as they are courted by bigger financial firms.

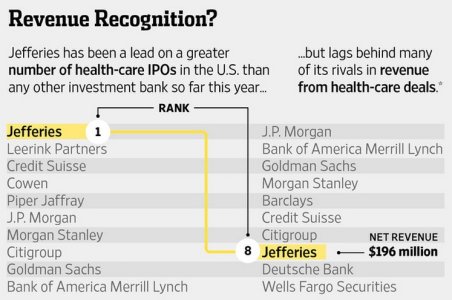

In 2014, Jefferies has been a lead underwriter on 25 U.S.-listed initial public offerings of health-care-related companies, topping all other investment banks, according to data provider Dealogic. But Jefferies ranks just eighth in net revenue generated by U.S. health-care banking overall—which includes stock and bond offerings, loans and merger advice—generating $196 million in revenue, trailing No. 1 J.P. Morgan Chase & Co.’s $639 million. “Investment banking has always been highly competitive,” Jefferies Chief Executive Richard Handler said in an interview at his office, just off the trading floor.

The firm isn’t attached to a bank holding company and therefore has more flexibility in how it structures deals and compensates employees. This entrepreneurial structure was part of the allure when Mr. Lorello moved to Jefferies in 2009 with more than 30 health-care bankers, according to people familiar with the firm. Jefferies is a unit of Leucadia National Corp. and has net revenue topping $3 billion.

“Our competitive advantage has never been stronger in the 25 years I have been at Jefferies,” Mr. Handler said.

Mr. Handler is particularly protective now. In an October memo to clients, he said rivals fanned rumors after Jefferies’s health-care chief, Sage Kelly, took a voluntary leave in October. In a custody dispute, Mr. Kelly’s wife accused the banker, along with some colleagues and clients, of drug use and claimed she was involved in a ***ual tryst with a Jefferies client. The firms denied the allegations, and Mr. Kelly’s wife has issued an apology. Mr. Kelly, 42 years old, remains on leave. Mr. Kelly declined to comment. Mr. Lorello, 61, who is running the health-care group in Mr. Kelly’s absence, couldn’t be reached for comment.

Mr. Handler said the health-care business hasn’t slowed. In the month since the episode erupted, the firm has been hired to work on 28 new health-care deals, he said.

Jefferies has about 90 people now focusing strictly on health care, spotting promising startups and pushing hard to win work from bigger companies. The group has accounted for nearly 22% of the firm’s U.S. investment-banking net revenue this year, according to Dealogic. Clients said Mr. Handler, 53, often is directly involved in deals.

“I don’t know the head of Deutsche Bank, but I know the chief executive of Jefferies,” said Tilman Fertitta, chief executive of Landry’s Inc., a $3 billion restaurant group that has worked closely with Mr. Lorello and other top executives.

During a financial crunch in February 2007, Landry’s had to refinance bonds. “The whole senior management team got involved and got it done,” Mr. Fertitta said. “I’ll never forget that.”

The involvement of top Jefferies executives helped the firm win business to manage Ardea Biosciences Inc.’s follow-on offerings of stock in 2010, 2011 and 2012. But when Ardea was acquired by AstraZeneca PLC in a roughly $1.3 billion deal in 2012, Ardea worked with Bank of America Merrill Lynch as financial adviser.

A Jefferies spokesman said a pre-existing merger-and-acquisition engagement with Bank of America Merrill Lynch led its bigger rival to win the Ardea deal. Jefferies, however, has continued to push hard and won subsequent work with Ardea executives when they formed a new company.

Among larger clients, Jefferies advised Valeant Pharmaceuticals International Inc. on its roughly $3.2 billion merger with Biovail Corp. announced in 2010. It has also advised Pfizer Inc. The firm has worked on 18 health-care deals bigger than $1 billion this year.

But sometimes it takes smaller roles with smaller fees. For representing Chiesi Farmaceutici SpA in its complete acquisition of Cornerstone Therapeutics Inc. announced in 2013, it received $800,000 in fees, compared with $2.9 million paid to Lazard Ltd. for representing Cornerstone. Jefferies said its fees were lower because it didn’t have to do as much work on the Chiesi side, partly because Chiesi already owned part of Cornerstone.

Meanwhile, bigger banks are courting Jefferies’s clients as those companies expand.

“We have never worked with another bank,” said Chris Tanner, chief financial officer of Cosmo Technologies Ltd., which was advised recently by Jefferies on a potential $2.7 billion deal with Salix Pharmaceuticals Ltd. (The deal was canceled.)

“We get calls from other banks all the time now,” he said.

")