Grandissimo! Ottimo!Ciao antoooo, ho fatto un po' di archeologia su Aixtron scorrendo i vari report annuali

L'azienda ha avuto una fase di crescita esplosiva dopo il 2009 a seguito della forte espansione della tecnologia LED nei monitor, televisori etc

Vedi l'allegato 3003898

A partire dal 2011 i ricavi cominciano a calare, con un vero e proprio crollo nel 2012 e margini che passano in negativo

Vedi l'allegato 3003901

Vedi l'allegato 3003902

Negli anni successivi i ricavi si attestano attorno ai 200 milioni, con l'azienda che continua a spendere su R&D attorno a 50-60 milioni. Per intenderci nel 2023 la spesa in R&D era di 90 milioni con ricavi di 650 milioni.

Vedi l'allegato 3003904

L'azienda naviga tra le difficoltà sino al 2016, poi nel 2017 vende o interrompe alcuni linee di produzione non profittevoli e comincia a imbarcare ricavi dagli investimenti fatti nel settore dell'elettronica di potenza.

Vedi l'allegato 3003908

A quel punto i ricavi del segmento elettronica di potenza cominciano letteralmente a decollare come si vede dal grafico già mostrato ieri

Vedi l'allegato 3003910

Anche l'elettronica di potenza è un business ciclico, ma se guardiamo alla mobilità elettrica e all'elettrificazione in generale (inverter, etc) credo che strutturalmente siamo appena agli albori di un fenomeno che prenderà sempre più piede.

In conclusione:

non mi sembra una azienda da comprare per non vendere mai, è piuttosto un business da seguire regolarmente vagliando cosa succede al suo mercato e come si comporta rispetto alla concorrenza. In questa fase io la trovo interessante da accumulare, sia come investimento a medio/lungo termine che opportunisticamente approfittando della sua volatilità

Grazie infine delle due segnalazioni Melexis e Elmos: me le studierò

Installa l'app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Nota: This feature may not be available in some browsers.

Stai usando un browser molto obsoleto. Puoi incorrere in problemi di visualizzazione di questo e altri siti oltre che in problemi di sicurezza. .

Dovresti aggiornarlo oppure usare usarne uno alternativo, moderno e sicuro.

Dovresti aggiornarlo oppure usare usarne uno alternativo, moderno e sicuro.

La Replica dei Cloni (PUNK WARS)

- Creatore Discussione Logica Punk

- Data di inizio

Più opzioni

Chi ha risposto?ps. tra l'altro vedo che un 15-20% dei ricavi proviene da after-sales....non male, presumo che man mano che il numero di macchine installate aumenterà questa forma di ricavo sarà sempre più ricorrente e utile nelle fasi di down-cycle.

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Terry Smith relaziona sulla gestione del suo fondo nel 2023. Sempre un piacere ascoltarlo

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Op. #48- 17/04/2023

Dopo la trimestrale, comincio a ricostruire la posizione su ASML

AMSTERDAM, April 17 (Reuters) - ASML (ASML.EQ), the largest supplier of equipment to computer chip makers, reported weaker than expected first-quarter new bookings on Wednesday, although sales to China held up despite U.S.-led restrictions.

Shares in Europe's biggest tech firm, which had risen 34% this year, were down 4.5% to 873.40 euros at 0741 GMT

The Dutch group is seeing a lull in demand for its most advanced machines, but gearing up for strong growth in 2025 due to strong demand for AI and memory chips, including from TSMC of Taiwan {1}, which makes chips for Nvidia and Apple.

For 2024, ASML kept its financial forecasts unchanged, with sales seen flat from 2023's 27.6 billion euros ($29.3 billion).

ASML dominates the market for lithography systems, machines that can cost hundreds millions of euros each and use light beams to help create microscopic circuitry. It is set to benefit from new chip plants planned with support from governments in Taiwan, South Korea, Japan, China and the United States.

New bookings in the first quarter were 3.6 billion euros, well below the 5.4 billion seen by analysts polled by Reuters.

"Although disappointing we would not read too much into it as order intake is notoriously lumpy," said ING analyst Marc Hesselink.

Sales of ASML's lithography systems to customers in China made up a record 49% of the total in the first quarter, or around 2 billion euros, the company said in an investor presentation published alongside the earnings.

In recent years, China has been ASML's third market after Taiwan and South Korea, and ahead of the United States.

Prezzo di acquisto in EUR: 871

Azioni: 2

Importo totale investito: EUR 1,642

I cloni non vengono incrementati perchè si utilizza la liquidità già in portafoglio

-------

Dopo la trimestrale, comincio a ricostruire la posizione su ASML

AMSTERDAM, April 17 (Reuters) - ASML (ASML.EQ), the largest supplier of equipment to computer chip makers, reported weaker than expected first-quarter new bookings on Wednesday, although sales to China held up despite U.S.-led restrictions.

Shares in Europe's biggest tech firm, which had risen 34% this year, were down 4.5% to 873.40 euros at 0741 GMT

The Dutch group is seeing a lull in demand for its most advanced machines, but gearing up for strong growth in 2025 due to strong demand for AI and memory chips, including from TSMC of Taiwan {1}, which makes chips for Nvidia and Apple.

For 2024, ASML kept its financial forecasts unchanged, with sales seen flat from 2023's 27.6 billion euros ($29.3 billion).

ASML dominates the market for lithography systems, machines that can cost hundreds millions of euros each and use light beams to help create microscopic circuitry. It is set to benefit from new chip plants planned with support from governments in Taiwan, South Korea, Japan, China and the United States.

New bookings in the first quarter were 3.6 billion euros, well below the 5.4 billion seen by analysts polled by Reuters.

"Although disappointing we would not read too much into it as order intake is notoriously lumpy," said ING analyst Marc Hesselink.

Sales of ASML's lithography systems to customers in China made up a record 49% of the total in the first quarter, or around 2 billion euros, the company said in an investor presentation published alongside the earnings.

In recent years, China has been ASML's third market after Taiwan and South Korea, and ahead of the United States.

Prezzo di acquisto in EUR: 871

Azioni: 2

Importo totale investito: EUR 1,642

I cloni non vengono incrementati perchè si utilizza la liquidità già in portafoglio

-------

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Aumentano sempre di più le patologie per le quali sono in corso sperimentazioni basate su farmaci antiobesità

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Op. #49- 18/04/2023

Incremento ASML

Prezzo di acquisto in EUR: 837

Azioni: 1

Importo totale investito: EUR 837

I cloni non vengono incrementati perchè si utilizza la liquidità già in portafoglio

-------

Incremento ASML

Prezzo di acquisto in EUR: 837

Azioni: 1

Importo totale investito: EUR 837

I cloni non vengono incrementati perchè si utilizza la liquidità già in portafoglio

-------

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

UPDATE 3-Hermes quarterly sales jump 17% on strong China demand

(Adds share price and analyst comment in paragraphs 5-7)By Mimosa Spencer

PARIS, April 25 (Reuters) - Birkin bag maker Hermes reported a 17% surge in first-quarter sales on Thursday, sustaining a rapid growth rate from the previous quarter including in China, and underlining strong demand for high end luxury.

Its first-quarter growth beat expectations and far outpaced larger rival LVMH , showing the strength of businesses operating in the top end of the market and defying broader weakness in key market China.

Sales rose to 3.81 billion euros ($4.08 billion) for the three months to March 31 and beat expectations for a 13% rise, according to consensus provider Visible Alpha.

One of the most consistent performers in the luxury goods sector, the fashion group is known for its ability to maintain strong growth even in the face of deteriorating economic conditions.

Hermes shares traded down 2.5% in late morning trading as investors who have benefited from an over 20% rise since the start of the year, took profits.

The consensus-beating sales figure was probably not a "major surprise" given the company's record over the past four years of exceptional growth and "consistent over-delivery on expecations," said Thomas Chauvet, analyst with Citi.

He highlighted, as an exception, a miss in expectations for the smaller watches division, which clocked 4% growth, compared to Citi's forecast for 11% growth.

Sales updates from several leading luxury groups including LVMH and Kering have offered little reassurance that Chinese demand for high-end fashion is bouncing back.

Consultancy Bain forecasts mid-single-digit percentage growth for China's luxury market this year, slowing from 12% growth in 2023, when business boomed following the lifting of COVID-related lockdowns.

Hermes, which sells handbags priced at more than $10,000, said its sales in Asia excluding Japan grew 14%, and all other regions reported double-digit rises.

The company saw "slightly softer" traffic in China in March following the Chinese New Year holiday, Hermes Executive Vice-President Finance Eric du Halgouet, told journalists.

However, strong demand from wealthier clients offset fewer store visits from clients seeking more affordable silk items and fashion accessories, he said.

"Our more well-off clients continued to visit our stores," said du Halgouet, noting that average spending was higher.

Globally, the leather goods division, the company's largest, grew by 20% in the quarter, driven by new models such as the Constance Elan bag.

After holding back when Chanel, LVMH-owned Dior and Louis Vuitton raised prices of their handbags more aggressively during the pandemic, Hermes started raising prices more significantly from last year.

This year's increase of 8% will provide it with a tailwind, said analysts at Bernstein.

Hermes has a higher valuation than rivals with a 12 month forward price-to-earnings ratio based on projected earnings of 51, according to LSEG data. That compares with LVMH at 24 and Kering at 16.

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Non piace al mercato la trimestrale di Autostore con ricavi in calo

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Op. #50 - 02/05/2024

Ad un P/E di 15, un PEG di 1,7, un ROIC di 21 ed un dividend yield di 4,4 entro su ROCHE Holding (ROG)

Lasciando da parte il discounted cahs flow di Simply Wall Street che la dà addirittura sottovalutata del 70%, se la sconto ad un onesto tasso di 10% e assumo una media di crescita del FCF del 4%, Roche mi risulta sottovalutata del 23%.

Nell'ultima trimestrale Roche vede una crescita del business base del 7%.

Una covid stock che sembra aver spurgato quasi tutto quello che doveva spurgare dall'hype pandemico, che ora inserisco nella mia strategia core

Prezzo di acquisto in EUR: 224,89

Azioni: 6

Importo totale investito: EUR 1,349

I cloni non vengono incrementati perchè si utilizza la liquidità già in portafoglio

-------

Ad un P/E di 15, un PEG di 1,7, un ROIC di 21 ed un dividend yield di 4,4 entro su ROCHE Holding (ROG)

Lasciando da parte il discounted cahs flow di Simply Wall Street che la dà addirittura sottovalutata del 70%, se la sconto ad un onesto tasso di 10% e assumo una media di crescita del FCF del 4%, Roche mi risulta sottovalutata del 23%.

Nell'ultima trimestrale Roche vede una crescita del business base del 7%.

Una covid stock che sembra aver spurgato quasi tutto quello che doveva spurgare dall'hype pandemico, che ora inserisco nella mia strategia core

Prezzo di acquisto in EUR: 224,89

Azioni: 6

Importo totale investito: EUR 1,349

I cloni non vengono incrementati perchè si utilizza la liquidità già in portafoglio

-------

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Op. #51 - 02/05/2024

Proseguiamo il riacquisto di ASML, venduta opportunisticamente alcune settimane fa tra i 900 e i 950 EUR

Prezzo di acquisto in EUR: 816

Azioni: 1

Importo totale investito: EUR 816

-------

Proseguiamo il riacquisto di ASML, venduta opportunisticamente alcune settimane fa tra i 900 e i 950 EUR

Prezzo di acquisto in EUR: 816

Azioni: 1

Importo totale investito: EUR 816

-------

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

E intanto Novo Nordisk continua a confermarsi

https://www.cnbc.com/2024/05/02/novo-nordisk-earnings-q1-2024-weogovy-sales-double.html

https://www.cnbc.com/2024/05/02/novo-nordisk-earnings-q1-2024-weogovy-sales-double.html

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Genmab Announces Financial Results for the First Quarter of 2024

May 2, 2024 at 5:02 PM CEST

May 2, 2024 Copenhagen, Denmark;

Interim Report for the First Quarter Ended March 31, 2024

Highlights

- The U.S. Food and Drug Administration (U.S. FDA) granted Priority Review for the supplemental Biologics License Application (sBLA) for EPKINLY® (epcoritamab-bysp) for the treatment of adult patients with relapsed or refractory follicular lymphoma (FL) after two or more lines of systemic therapy, with a Prescription Drug User Fee Act (PDUFA) target action date of June 28, 2024

- An additional Phase 3 clinical trial was initiated, evaluating epcoritamab in combination with rituximab and lenalidomide compared to chemoimmunotherapy in previously untreated follicular lymphoma

- The U.S. FDA accepted for Priority Review the sBLA seeking to convert the accelerated approval of Tivdak® (tisotumab vedotin-tftv) to full approval, for the treatment of patients with recurrent or metastatic cervical cancer with disease progression on or after first-line therapy

- Genmab announced the decision of its arbitration appeal under its daratumumab license agreement with Janssen Biotech, Inc. (Janssen)

- Genmab revenue increased 46% compared to the first quarter of 2023, to DKK 4,143 million

Financial Performance First Quarter of 2024

- Revenue was DKK 4,143 million for the first three months of 2024 compared to DKK 2,834 million for the first three months of 2023. The increase of DKK 1,309 million, or 46%, was primarily driven by higher DARZALEX® and Kesimpta® royalties achieved under our collaborations with Janssen and Novartis Pharma AG (Novartis), respectively, EPKINLY net product sales, and a milestone achieved under our collaboration with AbbVie.

- Royalty revenue was DKK 3,104 million in the first three months of 2024 compared to DKK 2,408 million in the first three months of 2023, an increase of DKK 696 million, or 29%. The increase in royalties was driven by higher net sales of DARZALEX and Kesimpta.

- Net sales of DARZALEX (daratumumab), including sales of the subcutaneous (SC) product (daratumumab and hyaluronidase-fihj, sold under the tradename DARZALEX FASPRO® in the U.S.) by Janssen were USD 2,692 million in the first three months of 2024 compared to USD 2,264 million in the first three months of 2023, an increase of USD 428 million or 19%.

- Total costs and operating expenses were DKK 3,342 million in the first three months of 2024 compared to DKK 2,417 million in the first three months of 2023. The increase of DKK 925 million, or 38%, was driven by the expansion of our product pipeline, EPKINLY post launch activities in the U.S. and Japan, the continued development of Genmab’s broader organizational capabilities and related increase in team members to support these activities, as well as profit-sharing amounts payable to AbbVie related to EPKINLY sales.

- Operating profit was DKK 801 million in the first three months of 2024 compared to DKK 417 million in the first three months of 2023.

- Net financial items resulted in income of DKK 915 million for the first three months of 2024 compared to an expense of DKK 151 million in the first three months of 2023. The increase of DKK 1,066 million was primarily driven by movements in USD to DKK foreign exchange rates impacting Genmab’s USD denominated cash and cash equivalents and marketable securities, with strengthening of the USD/DKK rate in the first three months of 2024 compared to the weakening of the USD/DKK rate in the first three months of 2023.

- April: Genmab and ProfoundBio, Inc. (ProfoundBio) announced that the companies have entered into a definitive agreement for Genmab to acquire ProfoundBio in an all-cash transaction. The acquisition will give Genmab worldwide rights to three candidates in clinical development, including rinatabart sesutecan (Rina-S), plus ProfoundBio’s novel antibody-drug conjugate (ADC) technology platforms. Genmab will acquire ProfoundBio for USD 1.8 billion in cash, payable at closing (subject to adjustment for ProfoundBio’s closing net debt and transaction expenses). The proposed transaction is expected to close in the first half of 2024. The closing of the proposed transaction is subject to the satisfaction of customary closing conditions.

Genmab is maintaining its 2024 financial guidance published on February 14, 2024.

Following the announcement of the proposed acquisition of ProfoundBio, Genmab’s operating expenses before expenses incurred by it in connection with the proposed transaction are now anticipated to be at or moderately above the upper end of the previously disclosed guidance range of DKK 12.4 -13.4 billion. The anticipated increase reflects the incremental R&D investment to support the advancement of ProfoundBio’s clinical programs, primarily Rina-S. Genmab’s revenue guidance is unchanged and expected to be in the previously disclosed guidance range of DKK 18.7 – 20.5 billion.

We expect to update our guidance no later than in connection with our second quarter 2024 earnings.

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Op. #51 - 02/05/2024

Incremento su Novo Nordisk

Prezzo di acquisto in EUR: 117,06

Azioni: 4

Importo totale investito: EUR 468

--------------------

Incremento su Novo Nordisk

Prezzo di acquisto in EUR: 117,06

Azioni: 4

Importo totale investito: EUR 468

--------------------

Black_Mirror

Nuovo Utente

- Registrato

- 5/12/22

- Messaggi

- 6

- Punti reazioni

- 6

Roche ho fatto un ingresso anche io, a livello tecnico è su un ottimo supporto, a livello fondamentale l'azienda continua a crescere bene e nel 2024 l'effetto negativo del covid dovrebbe diminuire drasticamente fino a sparire nel 2025. CI sono un paio di farmaci che stanno crescendo a ritmi vertiginosi e mi piace molto l'acquisizione di Carmot, è una bella bet nel settore Obesity, vediamo come andrà.

La reputo un buon connubio tra crescita e dividendo, soprattutto se riusciranno a tirar fuori qualcosa in ambito obesity.

La reputo un buon connubio tra crescita e dividendo, soprattutto se riusciranno a tirar fuori qualcosa in ambito obesity.

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Ho molta fiducia in tutto il settore healthcare in sè.Roche ho fatto un ingresso anche io, a livello tecnico è su un ottimo supporto, a livello fondamentale l'azienda continua a crescere bene e nel 2024 l'effetto negativo del covid dovrebbe diminuire drasticamente fino a sparire nel 2025. CI sono un paio di farmaci che stanno crescendo a ritmi vertiginosi e mi piace molto l'acquisizione di Carmot, è una bella bet nel settore Obesity, vediamo come andrà.

La reputo un buon connubio tra crescita e dividendo, soprattutto se riusciranno a tirar fuori qualcosa in ambito obesity.

Complici le guerre, l'inflazione, il forte innalzamento dei tassi e il tema AI che praticamente causa un'eclisse totale su tutto il resto, non ci si rende davvero conto di quanta innovazione è stata fatta in ambito scientifico in medicina. La convergenza tra genetica e nuove possibilità computazionali ha sulla carta un potenziale enorme. Per contro, a causa dei tassi alti, soffrono sia gli investimenti in dispostivi medicali che il biotech è questo si nota piuttosto bene sul mercato: tolte le eccezioni eccellenti (Lilly, Novo, Boston Scientific, etc) e cash machines tipo le assicurazioni sanitarie, il grosso del settore galleggia.

Ma la spinta di questa innovazione non si è fermata e soprattutto la popolazione mondiale invecchia sempre di più, cresce in numero ed ha maggiori disponibilità: curarsi sarà sempre più tema strutturale e da questo io mi aspetto dei ritorni che al momento il mercato non sta generalmente prezzando.

Il gioco interessante è a questo punto assemblarsi il proprio mini-ETF, una selezione concentrata di titoli con cui cercare di intercettare la parte migliore è più duratura di questo trend in formazione

Black_Mirror

Nuovo Utente

- Registrato

- 5/12/22

- Messaggi

- 6

- Punti reazioni

- 6

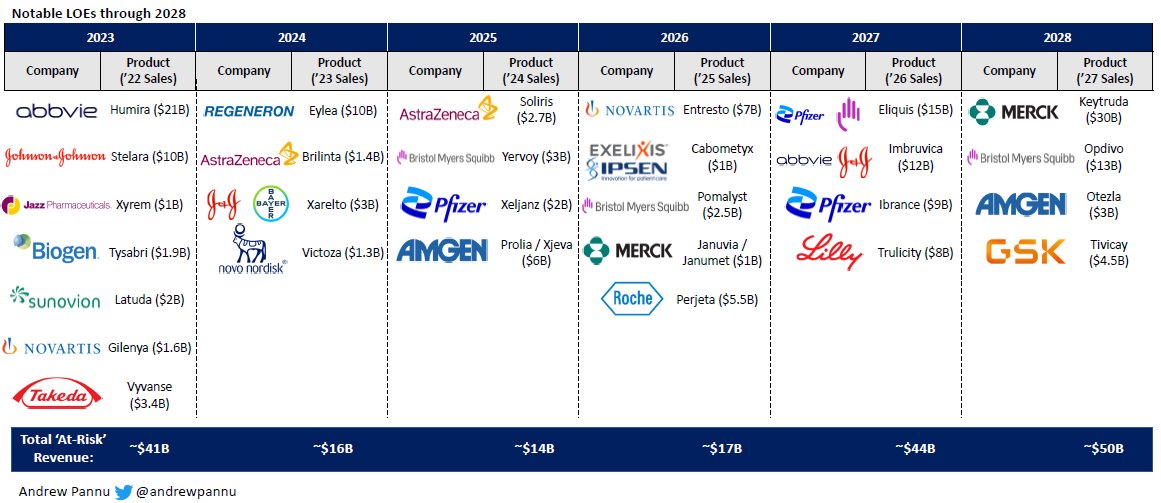

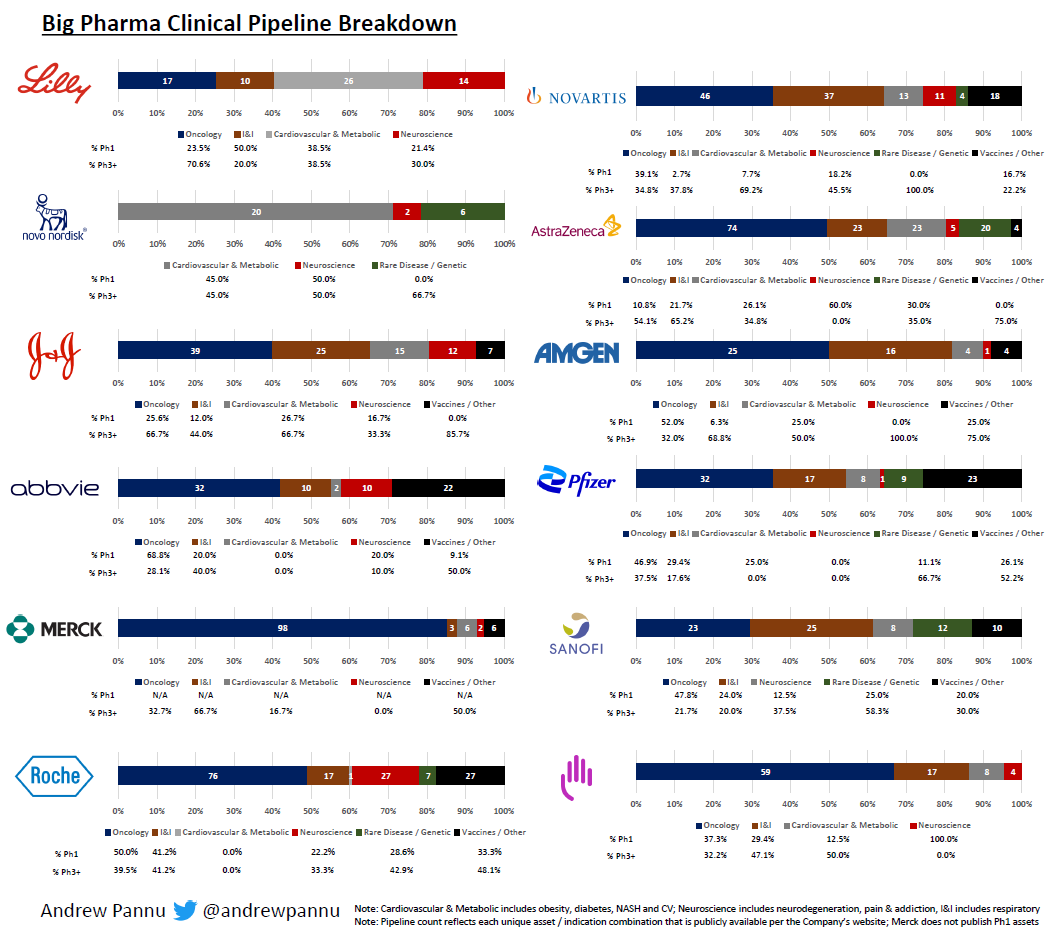

Un'altra pharma europea che possiedo e che reputo molto interessante è Sanofi. Tra le big è l'unica credo che non ha LOE rilevanti fino al 2030, ha un blockbuster (Dupixent) che dovrebbe arrivare a fatturare circa 20bn + diversi farmaci rilasciati da poco molto promettenti e una buona pipeline, sta inoltre investendo parecchio in AI. Valutazione e multipli ok.

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Davvero ottima questa grafica !!!!Un'altra pharma europea che possiedo e che reputo molto interessante è Sanofi. Tra le big è l'unica credo che non ha LOE rilevanti fino al 2030, ha un blockbuster (Dupixent) che dovrebbe arrivare a fatturare circa 20bn + diversi farmaci rilasciati da poco molto promettenti e una buona pipeline, sta inoltre investendo parecchio in AI. Valutazione e multipli ok.

Logica Punk

Fa un bollito con tanti ETF per il suo canarino

- Registrato

- 21/1/23

- Messaggi

- 1.524

- Punti reazioni

- 1.467

Mornigstar su CNH