Blacksmith.

AoK Heaven

- Registrato

- 26/4/16

- Messaggi

- 8.119

- Punti reazioni

- 1.195

nel comunicato inerente l'accelerazione ipotizzavano il 20 febbraio come ultimo trading day.

Eh, ma già avevo fatto notare che c'era l'incongruenza.

Il 21 febbraio verrà rimborsato il valore di chiusura di oggi o di domani?

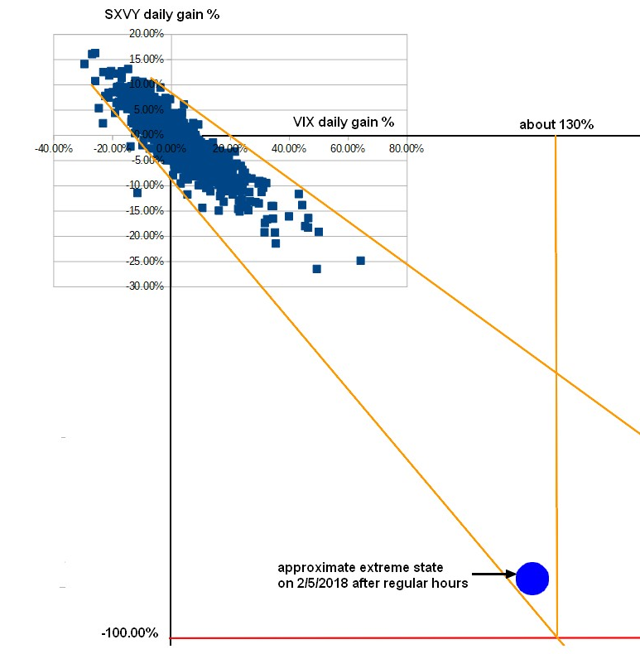

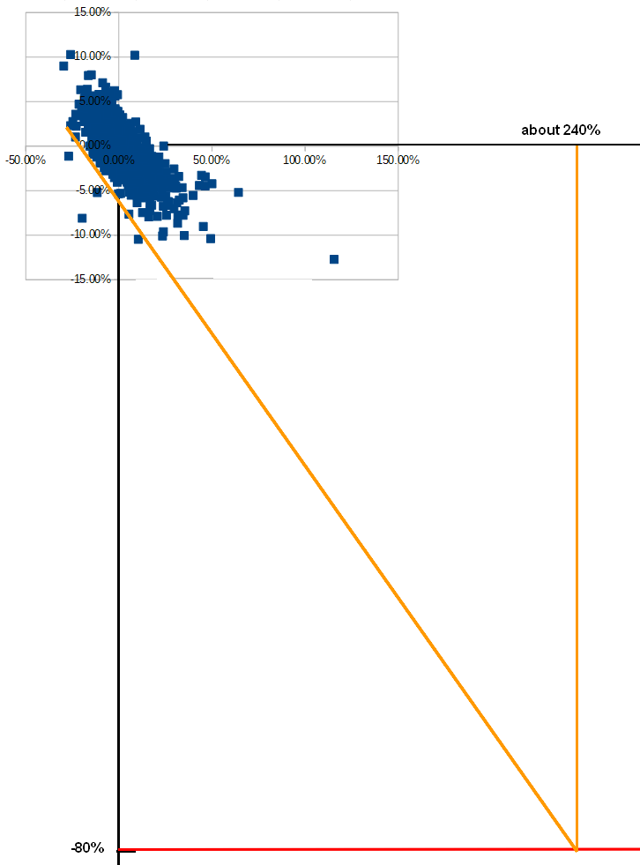

l'evento del 5 febbraio ha innescato le procedure che porteranno entro il 15 febbraio all'annuncio ufficiale (call notice) della data della call, che si prevede sarà il 21 febbraio, quando sarà rimborsato il valore di chiusura ufficiale del terzo giorno antecedente (16 febbraio).