Csiq

Posto qui sotto copia del p.m. inviato a chi me lo ha richiesto, con il suo assenso e con la speranza che possa essere di una qualsiasi utilità per chi legge.

giugin

CSIQ oggi ha aperto a 12.69 col segno +, dopo 15’ segnava con 12.42 il low di giornata (-2%), poi è tornato a crescere fino a rasentare la parità.

Facendo un giro d’orizzonte per questa società, osservo quanto segue.

Le vendite sono 377M nel Q3 2010 vs 213M nel Q3 2009 (+77%) e 329M nel Q2 2010 (+15%).

Il Gross Margin è il 17.3% nel Q3 2010 vs 16.3% nel Q3 2009 e 13.6% nel Q2 2010.

L’Operating Margin è il 10.6% nel Q3 2010 vs 9.3% nel Q3 2009 e 5.2% nel Q2 2010.

Il Net Margin è il 5.4% nel Q3 2010 vs 11.9% nel Q3 2009 e 0.9% nel Q2 2010.

L’EPS negli ultimi 7 Q ha avuto questa successione: -0.13, 0.49, 0.69, -0.38, 0.03, 0.07, 0.47.

Il “Cash & Equivalents” degli ultimi 5 Q è stato: 103M, 160M, 174M, 255M, 296M.

Il “Debito Totale” degli ultimi 5 Q è stato: 354M, 387M, 542M, 669M, 676M

La Cassa generata dall’attività operativa è stata 3.2M nell’anno 2008 e 50.9M nel 2009.

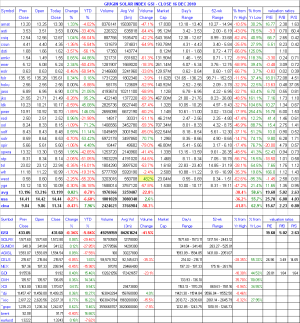

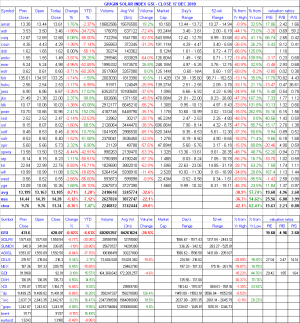

Per valutare come si classifica CSIQ all’interno del business solare, consideriamo i dati della Tab. E della mia weekly analysis sull’indice GSI, formato da 25 società “solari” (o prevalentemente tali).

Il Gross Margin (ttm) del GSI è 24.26% vs 13.57% di CSIQ.

L’Operating Margin (ttm) del GSI è 14.80% vs 4.83% di CSIQ. Occorre considerare però che solo 16 società (delle 25 del GSI) hanno un margine operativo positivo ed il 14.8% è la media del margine operativo delle sole 16 società “virtuose”.

Il Net Margin (ttm) del GSI è 8.40% vs 0.71% di CSIQ. Anche in questo caso, l’8.40% è la media del net margin delle sole 17 società aventi un utile positivo.

Il ROA, ROE, ROI del GSI valgono rispettivamente 7.65%, 17.89%, 11.91% vs 0.65%, 1.91%, 4.47% di CSIQ. Anche in questo caso, i valori del GSI sono medie calcolate solo su quei titoli che presentano valore positivo (sono 17 su 25).

Il Quick Ratio (mrq) del GSI vale 1.63 vs 1.08 di CSIQ, Il Current Ratio (mrq) del GSI vale 1.95 vs 1.30 di CSIQ.

Il rapporto debiti di lungo periodo/equity (mrq) del GSI vale 0.37 vs 0.12 di CSIQ. Il rapporto totale debiti/equity (mrq) del GSI vale 0.60 vs 1.42 di CSIQ.

Per il corporate efficiency (ttm) si ha che il rapporto fatturato/addetti per il GSI è 372M vs 183M di CSIQ; il rapporto utile netto/addetti per il GSI è 47M vs 7.2M del CSIQ (anche qui va precisato che il valore del GSI è calcolato considerando solo le società che hanno utile e non anche quelle che hanno perdita); il receivables turnover per GSI è 7.9 vs 7.2 per CSIQ; l’inventory turnover per GSI è 6 vs 6.3 per CSIQ; l’asset turnover per GSI è 0.8 vs 0.9 per CSIQ.

Da tutto quanto sopra scritto emerge che attualmente, considerando le risultanze di bilancio degli ultimi 4 trimestri e limitando il confronto con le migliori società (17 in totale) del GSI, Canadian Solar ha una posizione definibile come "marginale": si può dire che risulta fra le “peggiori delle migliori”.

Altro sembra emergere se consideriamo il trend di crescità di CSIQ, paragonando, come si è fatto all’inizio, i principali dati del Q3 2010 con quelli del Q3 2009 (confronto yoy cioè year over year) oppure con quelli del Q2 2010 (confronto qoq, cioè quarter over quarter).

CSIQ ha un range storico di prezzo che va dal max del 19.06.2008 (51.80) al min del 06.03.2009 (3.00). Mi sono divertito a “scaricare” ed ordinare (per closes decrescenti, ma se l’ordinamento lo faccio per “high” i cambiamenti sono minimi) la serie storica dei prezzi daily di CSIQ. Ebbene, il prezzo attuale (12.70) si colloca nel quinto decile del range di questa serie storica ordinata dei prezzi daily; se ti fa più comodo, ragioniamo in termini di “percentili”: il prezzo attuale (12.70) occupa il 47° percentile; in altre parole ancora, considerando tutti i prezzi daily assunti da CSIQ dal 09 novemtre 2006 ad ora (sono 1032), il 47% di essi è inferiore al prezzo attuale ed il 53% di essi è superiore al prezzo attuale. Insomma: non siamo messi proprio male!

E’ ovvio che, accanto a questa, occorre fare 1000 altre considerazioni per decidere consapevolmente se e quando uscire dalla posizione. Comunque i dati fondamentali li hai, come pure hai dati tecnici e quantitativi.

Io, sulla base di quanto qui scritto, mi terrei "stretto" il titolo, senza nessuna futura “mediazione al ribasso” fino al raggiungimento del punto di pareggio; poi stop loss trailing 2 deviazioni standard sotto ogni nuovo max (il titolo è fra i più volatili del GSI).

Questo è ciò che farei, senza consigliare a te nulla.

L'occasione mi è gradita per augurarti Buon Natale e Sereno 2011.

, and renewable resources.

, and renewable resources.