Ola kondor,

Per quanto riguarda il discorso secured?

credo sia poco importante per una società come Gtech...

.. allego quanto scritto da S&P

The following is a press release from Standard & Poor's: -- Italy-based GTECH S.p.A. intends to issue approximately $5 billion in new euro- and dollar-denominated secured notes to partially fund its intended $6.4 billion acquisition of International Game Technology (IGT). -- We are lowering our corporate credit ratings on GTECH and IGT to 'BB+' from 'BBB-' and removing them from CreditWatch negative. -- We are assigning our 'BB+' corporate credit rating to Georgia Worldwide PLC, the entity that will be the ultimate parent of GTECH and IGT once the acquisition closes. -- We are assigning our 'BB+' issue-level rating to Georgia Worldwide's proposed $5 billion in new senior secured notes. -- We are assigning our 'BB+' issue-level rating to GTECH's new $2.6 billion senior revolving credit facility due 2019, and its new EUR800 million senior term loan due 2019. -- We are lowering our issue-level ratings on GTECH and IGT's existing notes by one notch, in line with the lowering of the corporate credit ratings. -- The stable rating outlook reflects our expectation for relatively stable operating performance through 2016 and that adjusted debt to EBITDA will be in the high-4x area in 2016, in line with our current aggressive financial risk assessment and 'BB+' rating on Georgia Worldwide. NEW YORK (Standard & Poor's) Jan. 30, 2015--Standard & Poor's Ratings Services today said it assigned its 'BB+' corporate credit rating to U.K.-based Georgia Worldwide PLC. We expect this entity to be the parent of both GTECH S.p.A. and International Game Technology (IGT) once GTECH closes its acquisition of IGT. The rating outlook is stable. At the same time, we lowered our corporate credit ratings on GTECH and IGT to 'BB+' from 'BBB-', reflecting a consolidated view of the companies as wholly-owned subsidiaries of Georgia Worldwide. We removed the corporate credit ratings from CreditWatch with negative implications, where we had placed them on July 16, 2014. We also took the following issue-level rating actions: -- We assigned our 'BB+' issue-level rating to Georgia Worldwide's proposed $5 billion in senior secured notes. The recovery rating on these notes is '3'. -- We assigned our 'BB+' issue-level rating to GTECH's new $2.6 billion senior revolving credit facility (consisting of a $1.5 billion tranche and an EUR850 million tranche) due 2019, and its new EUR800 million senior term loan due 2019. The recovery rating on these loans is '3'. -- We lowered our issue-level ratings on GTECH's existing senior unsecured notes due 2018 and 2020 to 'BB+' from 'BBB-'. The recovery rating on these notes is '3'. -- We lowered our issue-level ratings on IGT's existing senior unsecured notes to 'BB+' from 'BBB-'. The '3' recovery rating on these and the above notes reflects our expectation for meaningful recovery (50% to 70%) for lenders in the event of a payment default. -- We lowered our issue-level rating on GTECH's subordinated debt to 'B+' from 'BB', three notches lower than the corporate credit rating given subordination and interest deferability of the notes. The recovery rating on this debt is '6', reflecting our expectation for negligible recovery (0% to 10%) for lenders in the event of a payment default. Our 'BBB-' issue-level rating on IGT's $1.0 billion revolving credit facility remains unchanged because we believe this facility will be fully refinanced through capacity under GTECH's existing revolving credit facility, once the acquisition closes. The issue-level rating remains on CreditWatch with negative implications, however, given the possibility that the transaction will not close as anticipated. We expect proceeds from the new debt issues will be used to help fund the approximately $3.5 billion cash consideration to IGT shareholders, to fund EUR378 million in withdrawal rights, and to pay for refinancing and transaction fees and expenses. If the transaction closes as expected, we plan to withdraw our issue-level rating on IGT's revolving credit facility as well as our corporate credit rating on GTECH SpA, which will merge into Georgia Worldwide. "The one-notch downgrade of GTECH and IGT to 'BB+' reflects our expectation that adjusted debt to EBITDA of the consolidated entity (Georgia Worldwide) will increase to and remain in the high-4x area through 2016, from the mid-2x area for both GTECH and IGT," said Standard & Poor's credit analyst Ariel Silverberg. The increase in leverage is due largely to the approximately $3.5 billion cash payment expected to be paid to IGT shareholders as consideration for GTECH's acquisition of IGT, and by other acquisition-related expenses including a EUR378million payment to certain GTECH shareholders who elected to, as permitted under Italian law, put their shares back to the company at a specific price. Notwithstanding our reassessment of the combined entity's business risk profile as "strong," adjusted debt to EBITDA in the high-4x area is aligned with an "aggressive" financial risk profile and a 'BB+' corporate credit rating. The stable outlook reflects our expectation for relatively stable operating performance through 2016 and that adjusted debt to EBITDA will be in the high-4x area in 2016, in line with our current "aggressive" financial risk assessment and 'BB+' rating on Georgia Worldwide. We could raise the ratings if we expected adjusted debt to EBITDA to improve to and be maintained below 4x. An improvement in leverage to this level would require over 20% EBITDA growth in the next few years, relative to our current forecast, or a meaningful reduction in debt. We could lower the ratings if the company sustains adjusted leverage above 5x over the next few years. This would likely result from the company's inability to fully achieve, or delays in fully achieving, our level of forecasted synergies; from costs to achieve synergies that are meaningfully higher than we expect; or from inefficiencies due to integration that result in slower-than-expected EBITDA growth. Although less likely, we could lower the ratings if there are meaningful contract losses, which could cause us to lower our business risk assessment.

</pre>

Settimana di risk-off per i principali indici per via dei timori legati all’inflazione persistente e alle prospettive di tassi ancora elevati a lungo. Anche se il report di oggi sull’indice core Pce, la misura molto gradita alla Fed per valutare l’inflazione, ha mostrato un parziale raffreddamento, o quantomeno una stabilità. L’indice ha riportato una crescita su base annua del 2,8%, in linea con le previsioni degli analisti e con la rilevazione del mese precedente. Questo dovrebbe lasciare più margine di manovra alla Fed per abbassare i tassi di interesse nel corso del 2024. Passando al Vecchio Continente, il report sull’inflazione dell’Eurozona ha mostrato un indice al 2,6%, oltre il 2,5% atteso e in accelerazione rispetto al 2,4% precedente.

Settimana di risk-off per i principali indici per via dei timori legati all’inflazione persistente e alle prospettive di tassi ancora elevati a lungo. Anche se il report di oggi sull’indice core Pce, la misura molto gradita alla Fed per valutare l’inflazione, ha mostrato un parziale raffreddamento, o quantomeno una stabilità. L’indice ha riportato una crescita su base annua del 2,8%, in linea con le previsioni degli analisti e con la rilevazione del mese precedente. Questo dovrebbe lasciare più margine di manovra alla Fed per abbassare i tassi di interesse nel corso del 2024. Passando al Vecchio Continente, il report sull’inflazione dell’Eurozona ha mostrato un indice al 2,6%, oltre il 2,5% atteso e in accelerazione rispetto al 2,4% precedente.

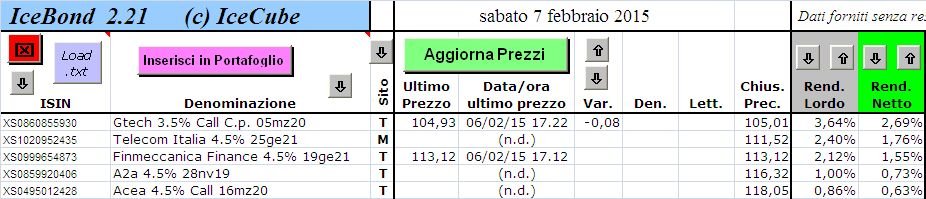

e guarda cosa rendono i suoi bond

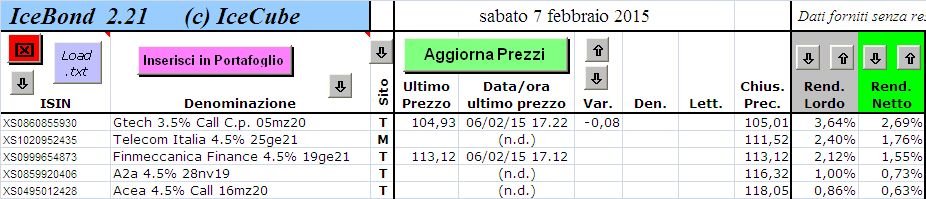

e guarda cosa rendono i suoi bond