Installa l'app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Nota: This feature may not be available in some browsers.

Stai usando un browser molto obsoleto. Puoi incorrere in problemi di visualizzazione di questo e altri siti oltre che in problemi di sicurezza. .

Dovresti aggiornarlo oppure usare usarne uno alternativo, moderno e sicuro.

Dovresti aggiornarlo oppure usare usarne uno alternativo, moderno e sicuro.

titoli di stato - aste

- Creatore Discussione slowdown

- Data di inizio

Più opzioni

Chi ha risposto?

Australia c.bank meets, may start world rates rise

By Colin Brinsden

SYDNEY, Nov 4 (Reuters) - The Reserve Bank of Australia was meeting on Tuesday as financial markets speculated it could be the first major central bank to start a global trend of higher interest rates.

Many economists think the central bank will hold off on a rate move until December, although another robust month for Australia's hot property sector and strong U.S. growth numbers have prompted some predictions of a rise in official rates this week.

The Reserve Bank will announce its decision at 9:30 a.m. (2230 GMT) on Wednesday.

A Reuters poll of 21 economists taken on Friday, before Monday's stronger-than-expected retail sales data, found 10 expected a rate hike in November or December, double the number in a similar poll a month ago.

All but two expected the central bank to raise the historically low cash rate, now 4.75 percent, by the end of March.

"Accommodative monetary policy has stood it in good stead for some time. It's been appropriate over the last year and a half or so but increasingly you no longer need stimulatory policy," said National Australia Bank head of market economics Tony Pearson.

"The pressure for that move to start in the next few months is rising a lot," he said.

The cash rate will have stood at 4.75 percent for 17 months if the Reserve Bank chooses to hold fire again. Unlike other central banks the Reserve Bank has not eased rates since tightening in May and June of last year.

Bank bill futures, which reflect market expectations on interest rate levels, were stable after taking a tumble on Monday's strong Australian data. Falling futures prices indicate increased expectations of higher interest rates.

December futures were at 94.82, unchanged from Monday and implying 90-day bill rates of 5.18 percent next month.

PIPPING THE BANK OF ENGLAND

Central banks around the world have been cutting rates to try to lift their economies out of a slump, but recently there have been signs of a rosier outlook.

The Bank of England's policy-making committee meets later this week and is also thought to be considering a tightening of monetary policy. The British central bank's key lending rate is at 3.5 percent, a 48-year low.

That said, the world's economic powerhouse, the United States, has said it will keep interest rates low for some time yet.

The Australian poll gave a 30 percent chance of a November hike, with many analysts suggesting the central bank would use its November 10 quarterly statement to prepare investors for an impending tightening cycle.

The bank makes no comment when it leaves rates unchanged.

Financial markets have priced in a rate hike by end-December for some time. But as evidence of Australian economic strength has mounted, they have begun to factor in the risk of two quarter-point moves this year or one half-point rise.

While high by international standards, lending rates are the lowest Australians have seen in around three decades. With unemployment at a 13-year low, consumers have been snapping up property and borrowing at unprecedented levels to buy cars and furniture.

The RBA has long talked of its concern that too many investors have bought property, saying large returns cannot last.

However, house prices rose 18 percent in the year to June and central bank data on Friday showed credit for housing leapt 2.1 percent in September -- a 22.5 percent increase in the year and the highest level since October 1994.

"They've been jawboning it for the last 18 months or so. Eventually, if you don't start to back your rhetoric with action people know it's hollow," said National Australia's Pearson.

(Additional reporting by Miranda Maxwell) ((Editing by Adam Cox; colin.brinsden@reuters.com; Reuters Messaging: colin.brinsden.reuters.com@reuters.net; +61-2-9373-1818))

Copyright 2000 Reuters Limited.

By Colin Brinsden

SYDNEY, Nov 4 (Reuters) - The Reserve Bank of Australia was meeting on Tuesday as financial markets speculated it could be the first major central bank to start a global trend of higher interest rates.

Many economists think the central bank will hold off on a rate move until December, although another robust month for Australia's hot property sector and strong U.S. growth numbers have prompted some predictions of a rise in official rates this week.

The Reserve Bank will announce its decision at 9:30 a.m. (2230 GMT) on Wednesday.

A Reuters poll of 21 economists taken on Friday, before Monday's stronger-than-expected retail sales data, found 10 expected a rate hike in November or December, double the number in a similar poll a month ago.

All but two expected the central bank to raise the historically low cash rate, now 4.75 percent, by the end of March.

"Accommodative monetary policy has stood it in good stead for some time. It's been appropriate over the last year and a half or so but increasingly you no longer need stimulatory policy," said National Australia Bank head of market economics Tony Pearson.

"The pressure for that move to start in the next few months is rising a lot," he said.

The cash rate will have stood at 4.75 percent for 17 months if the Reserve Bank chooses to hold fire again. Unlike other central banks the Reserve Bank has not eased rates since tightening in May and June of last year.

Bank bill futures, which reflect market expectations on interest rate levels, were stable after taking a tumble on Monday's strong Australian data. Falling futures prices indicate increased expectations of higher interest rates.

December futures were at 94.82, unchanged from Monday and implying 90-day bill rates of 5.18 percent next month.

PIPPING THE BANK OF ENGLAND

Central banks around the world have been cutting rates to try to lift their economies out of a slump, but recently there have been signs of a rosier outlook.

The Bank of England's policy-making committee meets later this week and is also thought to be considering a tightening of monetary policy. The British central bank's key lending rate is at 3.5 percent, a 48-year low.

That said, the world's economic powerhouse, the United States, has said it will keep interest rates low for some time yet.

The Australian poll gave a 30 percent chance of a November hike, with many analysts suggesting the central bank would use its November 10 quarterly statement to prepare investors for an impending tightening cycle.

The bank makes no comment when it leaves rates unchanged.

Financial markets have priced in a rate hike by end-December for some time. But as evidence of Australian economic strength has mounted, they have begun to factor in the risk of two quarter-point moves this year or one half-point rise.

While high by international standards, lending rates are the lowest Australians have seen in around three decades. With unemployment at a 13-year low, consumers have been snapping up property and borrowing at unprecedented levels to buy cars and furniture.

The RBA has long talked of its concern that too many investors have bought property, saying large returns cannot last.

However, house prices rose 18 percent in the year to June and central bank data on Friday showed credit for housing leapt 2.1 percent in September -- a 22.5 percent increase in the year and the highest level since October 1994.

"They've been jawboning it for the last 18 months or so. Eventually, if you don't start to back your rhetoric with action people know it's hollow," said National Australia's Pearson.

(Additional reporting by Miranda Maxwell) ((Editing by Adam Cox; colin.brinsden@reuters.com; Reuters Messaging: colin.brinsden.reuters.com@reuters.net; +61-2-9373-1818))

Copyright 2000 Reuters Limited.

Questo articolo, segnalato in altro post , lo riporto perchè potrebbe essere utile (per me lo è) a cercare di capire alcune cose che trovo difficili da far quadrare in relazione al tema "tassi".

E' lungo ma ne vale la pena

Contradictions: The Fed vs. the Bond Market

By: John Mauldin, Millennium Wave Advisors

Fannie and Freddie Distort the Market

The Fed Hits the Brakes

Contradictions: The Fed vs. the Bond Market

Where's the Market Discipline?

Even More Contradictions

Two weeks ago we examined the changes in our lives. Last week we looked at imbalances in the economy. This week the theme that I see in my daily reading is the large number of major contradictions apparent in the markets. There are so many contradictions we will not get to them all, but let's start, as it will make for some interesting and controversial analysis.

Fannie and Freddie Distort the Market

The main contradiction we will deal with starts with a lunch conversation I had with bond market analysts and guru Jim Bianco two weeks ago in Chicago. Jim is one of the smartest analysts I know and is a fascinating font of information.

We were talking hedge and macro funds, and he asked me what I thought was the best "trade" I saw. I answered that for aggressive traders, I liked the Eurodollar options. I will explain them in more detail below, but they are pricing in a Fed interest rate rise of over 1.75% by December 2004, which is just 14 months from now. I opined as how I did not think there is a significant chance of such a magnitude of a raise actually happening, and that I could not understand how the bond market could actually believe the Fed would raise rates that fast.

Jim replied, "They don't. The Eurodollar futures mis-pricing is a result of Fannie Mae and Freddie Mac distorting the market." As he explained his reasoning, and as I have thought about it since then, I think he may have an answer for part of the puzzling contradiction between what the Fed is saying and what the market is pricing.

First, the Fed cannot be any clearer about their intention to keep short term rates low. A "considerable" period is how they term it. One Fed governor told us a few weeks ago that a considerable period is 18 months. That is past the end of 2004.

Typical is what influential San Francisco Fed President Robert Parry, the second longest serving Fed policymaker, had to say:

"The rise in long-term interest rates since summer has already taken the wind out of the refinancing boom, which put so much money in people's pockets. Core inflation, which is already under 1.5%, may slip even lower. The recent period of weak investment demand has not only led to a fall in inflation, but it has also depressed economic activity.

"Thus, there is less concern about surprises that could push the inflation rate up, and more concern about surprises that could push the inflation rate lower, possibly even leading to deflation."

For now, let's simply take the Fed at its word that rate increases are not in the near term future. Except that the bond market seemingly does not take the Fed at its word, nor do the futures market imply anything close to trust or belief. My "favorite" trade I mentioned to Jim got crushed this week. There are two ways to bet on or hedge interest rate risk and direction. You can invest in Fed fund futures or Eurodollar futures. (Fed fund futures are typically used for shorter term moves and Eurodollar futures are used for longer term hedging. That is because after a duration of about one year, the Fed funds futures markets are not very liquid or sizeable, and the Eurodollar markets are where the huge action is, as we will see.)

The September '04 Eurodollar contract implies that the Fed will raise rates by 1.25 % over the next 11 months. If you go to December '04, rates are expected to rise by 1.71% and if you go to December 2006, the market apparently thinks short term Fed fund rates will be 4.96%, almost a full 4% rise. Can you say 9.5-10% mortgage rates, boys and girls? That also implies that inflation plus growth will be well north of 6-7%.

But wait, there is an odd fact within the very markets. If you go to the Fed funds rate for August of '04, there you find that rates are expected to rise only 0.75%. The market is saying that just one month later rates will rise by a full half percent.

The market is saying that Alan Greenspan is going to raise rates by 0.5% just 45 days in advance of what will be a very close presidential election (on top of the 0.75% they think he will have raised by August). Further, the market is implying that the economy, or inflation, or both will be so strong that Greenspan will have no choice but to do so.

I am not going to dispute that the economy is not growing strongly. It clearly is. It could grow at an above trend pace for well into next year. That makes me happy. But I think there is some inherent weakness in this recovery that makes it more suspect than others recoveries we have experienced since the end of WW2. As we will see, I find it hard to believe that there is something in the economic water that could cause Greenspan to raise rates 45 days in front of an election.

Let's go to my favorite macro analyst, Greg Weldon, and look at some of the data he slices and dices in his latest Money Monitor, arguing that there are no rate increases in our future. (www.macro-strategies.com)

"Bottom Line: over the last FOUR months, the annualized rate of decline in US Average Weekly Earnings is (-) 1%. Without income reflation [growth in personal income], there is virtually NO ladder for inflation to climb, ESPECIALLY under the auspices of CONTRACTING money supply." (quote with edits) Think about that. No growth in income in the strongest quarter in many a year.

"... without income gains, wealth reflation will be the SOLE support going into an election year." By wealth reflation, Weldon means stock market and housing price gains. Yet that might be in jeopardy as the Fed actually appears to be tapping on the brakes by tightening the money supply.

The Fed Hits the Brakes

He documents at length the significant recent slow down of growth of M-2 and M-3. He asks: "CAN wealth reflation in the US withstand the TIGHTEST monetary conditions since the last great stock-market wealth DEFLATION ??? ....with the tightest monetary stance via long-term-of-short-term M3, since 1997."

Then he offers this very interesting data from the Philadelphia Fed Survey:

"While ALL the focus was on the admittedly robust OUTPUT data, we note the less-focused-upon "Special Question" segment of the survey, which asked:

If you experienced a decline in Production during the 2001 Recession (72.5% of all, did), has Production returned to pre-2001 levels?85.7% replied NO.

Then, If not (85.7% of the 72.5%), WHEN do you expect Production to return to pre-2001 levels?53.1% said between 2Q-4Q 2004 ... BUT the rest, over 43%, said "Not in the Foreseeable Future".

"Indeed, nearly a THIRD of ALL firms stated that Production is NOT likely to regain pre-2001 levels. YET, money supply [growth] is trending well BELOW the degree of stimulus that was on the offer, since pre-2001.

"FAR WORSE, in the macro-secular sense, is this final tidbit from the 'Special Question' segment of the Philly Fed:

"23.4% of the 85.7% of ALL firms that originally stated that Production had not reached back to pre-recession levels, said they did NOT expect Production to reach back to pre-2001 levels ...BECASUSE of ... "Long-term Decline in the Industry."

"Indeed, note the Fed's own text ... 'Moreover, a large percentage of firms (44 percent) do not expect production to return to those pre-recession levels in the foreseeable future, for reasons involving competitiveness or longterm declines in their industries.'"

"YEAH, [he writes sarcastically] lets TRIPLE the Fed Funds rate!!!"

The headlines you read talk about how jobs are getting better. If you look at initial claims, you might get that idea. They are below the psychologically important 400,000 and are dropping ever so slowly. Comparing the real numbers with last year, there is a slight improvement, which is good.

But Continuing Claims are rising, and back to levels seen earlier this year. Taken together, this means that fewer people are losing their jobs, but fewer are also finding jobs.

Let's reflect upon that for a moment. We are told the economy grew by something like 6% in the third quarter. That means with inflation we are talking a nominal rate of over 7% and maybe 8%. That is as powerful as it has been for a long time.

And yet, no jobs. No income growth. As Weldon notes elsewhere, only 2% of those firms surveyed said they were paying lower prices, with 25% paying higher prices, yet 72% say they have no pricing power and are unable to raise prices.

Let's look at where the out-sized growth came from last quarter. Stephen Roach tells us 2% of real GDP growth came from automobile sales in the last two quarters. Consumers, supplied with a tax cut and massive home equity financing from the second quarter as rates briefly dropped to historical lows, took the heavy incentive deals they were offered on cars which were also priced lower than this time last year.

"Surging expenditures on consumer durables [mostly automobiles] accounted for about 2.0 percentage points of annualized real GDP growth, alone, over the past two quarters. To the extent that such an impetus did not reflect the fundamentals of pent-up demand, a payback of like magnitude would not be surprising. Historical experience does, in fact, tell us that's the norm after any spike in durables spending -- let alone the excessive one of the past two quarters. Since 1960, there have been 16 instances of excessive growth in durable goods consumption (defined as an annualized growth contribution exceeding 1.5 percentage points of real GDP) that contributed, on average, 2.2 percentage points of annualized real GDP growth; in the two quarters that followed, the growth contribution slowed dramatically, on average, to just 0.1 percentage point. To the extent such a payback is likely after the current spending burst, it could act as a sharp depressant on overall demand growth in subsequent quarters. That development, in the context of a lingering jobless recovery, could raise serious questions about the staying power of America's current cyclical resurgence." (Stephen Roach of Morgan Stanley)

Could auto sales maintain this level for one more quarter? Perhaps, as small business people all over America come to the end of the year and realize that under the current tax code, if they buy an SUV which weighs over 6,000 pounds (Lincoln Navigator, Cadillac Escalade, Lexus, Chevrolet, Ford, etc,) they may be able to deduct the entire cost from their 2003 taxes. In essence, the government just made these monsters more affordable than smaller cars at two-thirds the price.

(Yes, to my shocked readers in Europe, a 1986 tax rule provides that small businesses can deduct the cost of commercial vehicles, which are defined as small trucks which weigh over 6,000 pounds, which in the US includes large SUVs. The Bush tax stimulus package allows small businesses to deduct up to $100,000 of capital business expenditures immediately per year, up from $25,000 if I remember right. The idea was to get businesses to buy more computers and equipment and furniture, etc. Under the current rules, SUVs also fit into this category. Only in America.)

The good news is that the US economy apparently grew 6% in the third quarter of this year, and should do well this quarter and into the New Year. But this is a stimulus led recovery, and where will the next shove come from? The Bush administration has to hope that oil will drop to around $20, or that rates will somehow come back down.

Roach says, and I agree, "Eager to jump-start the US economy prior to the upcoming presidential election, the Bush Administration focused on front-loaded tax cuts that were designed to have maximum impact in 2004. "Spring-loaded" was the term used by Treasury Secretary John Snow to describe the growth potential of these measures. Well, the White House may have gotten more than it bargained for. The risk, in my view, is that the policy induced stimulus occurred sooner than expected in 2003 -- leaving the US economy having to face the "air-pocket" of a payback in early 2004. Needless to say, that would come during a period of maximum vulnerability insofar as the election cycle is concerned."

---- continua

E' lungo ma ne vale la pena

Contradictions: The Fed vs. the Bond Market

By: John Mauldin, Millennium Wave Advisors

Fannie and Freddie Distort the Market

The Fed Hits the Brakes

Contradictions: The Fed vs. the Bond Market

Where's the Market Discipline?

Even More Contradictions

Two weeks ago we examined the changes in our lives. Last week we looked at imbalances in the economy. This week the theme that I see in my daily reading is the large number of major contradictions apparent in the markets. There are so many contradictions we will not get to them all, but let's start, as it will make for some interesting and controversial analysis.

Fannie and Freddie Distort the Market

The main contradiction we will deal with starts with a lunch conversation I had with bond market analysts and guru Jim Bianco two weeks ago in Chicago. Jim is one of the smartest analysts I know and is a fascinating font of information.

We were talking hedge and macro funds, and he asked me what I thought was the best "trade" I saw. I answered that for aggressive traders, I liked the Eurodollar options. I will explain them in more detail below, but they are pricing in a Fed interest rate rise of over 1.75% by December 2004, which is just 14 months from now. I opined as how I did not think there is a significant chance of such a magnitude of a raise actually happening, and that I could not understand how the bond market could actually believe the Fed would raise rates that fast.

Jim replied, "They don't. The Eurodollar futures mis-pricing is a result of Fannie Mae and Freddie Mac distorting the market." As he explained his reasoning, and as I have thought about it since then, I think he may have an answer for part of the puzzling contradiction between what the Fed is saying and what the market is pricing.

First, the Fed cannot be any clearer about their intention to keep short term rates low. A "considerable" period is how they term it. One Fed governor told us a few weeks ago that a considerable period is 18 months. That is past the end of 2004.

Typical is what influential San Francisco Fed President Robert Parry, the second longest serving Fed policymaker, had to say:

"The rise in long-term interest rates since summer has already taken the wind out of the refinancing boom, which put so much money in people's pockets. Core inflation, which is already under 1.5%, may slip even lower. The recent period of weak investment demand has not only led to a fall in inflation, but it has also depressed economic activity.

"Thus, there is less concern about surprises that could push the inflation rate up, and more concern about surprises that could push the inflation rate lower, possibly even leading to deflation."

For now, let's simply take the Fed at its word that rate increases are not in the near term future. Except that the bond market seemingly does not take the Fed at its word, nor do the futures market imply anything close to trust or belief. My "favorite" trade I mentioned to Jim got crushed this week. There are two ways to bet on or hedge interest rate risk and direction. You can invest in Fed fund futures or Eurodollar futures. (Fed fund futures are typically used for shorter term moves and Eurodollar futures are used for longer term hedging. That is because after a duration of about one year, the Fed funds futures markets are not very liquid or sizeable, and the Eurodollar markets are where the huge action is, as we will see.)

The September '04 Eurodollar contract implies that the Fed will raise rates by 1.25 % over the next 11 months. If you go to December '04, rates are expected to rise by 1.71% and if you go to December 2006, the market apparently thinks short term Fed fund rates will be 4.96%, almost a full 4% rise. Can you say 9.5-10% mortgage rates, boys and girls? That also implies that inflation plus growth will be well north of 6-7%.

But wait, there is an odd fact within the very markets. If you go to the Fed funds rate for August of '04, there you find that rates are expected to rise only 0.75%. The market is saying that just one month later rates will rise by a full half percent.

The market is saying that Alan Greenspan is going to raise rates by 0.5% just 45 days in advance of what will be a very close presidential election (on top of the 0.75% they think he will have raised by August). Further, the market is implying that the economy, or inflation, or both will be so strong that Greenspan will have no choice but to do so.

I am not going to dispute that the economy is not growing strongly. It clearly is. It could grow at an above trend pace for well into next year. That makes me happy. But I think there is some inherent weakness in this recovery that makes it more suspect than others recoveries we have experienced since the end of WW2. As we will see, I find it hard to believe that there is something in the economic water that could cause Greenspan to raise rates 45 days in front of an election.

Let's go to my favorite macro analyst, Greg Weldon, and look at some of the data he slices and dices in his latest Money Monitor, arguing that there are no rate increases in our future. (www.macro-strategies.com)

"Bottom Line: over the last FOUR months, the annualized rate of decline in US Average Weekly Earnings is (-) 1%. Without income reflation [growth in personal income], there is virtually NO ladder for inflation to climb, ESPECIALLY under the auspices of CONTRACTING money supply." (quote with edits) Think about that. No growth in income in the strongest quarter in many a year.

"... without income gains, wealth reflation will be the SOLE support going into an election year." By wealth reflation, Weldon means stock market and housing price gains. Yet that might be in jeopardy as the Fed actually appears to be tapping on the brakes by tightening the money supply.

The Fed Hits the Brakes

He documents at length the significant recent slow down of growth of M-2 and M-3. He asks: "CAN wealth reflation in the US withstand the TIGHTEST monetary conditions since the last great stock-market wealth DEFLATION ??? ....with the tightest monetary stance via long-term-of-short-term M3, since 1997."

Then he offers this very interesting data from the Philadelphia Fed Survey:

"While ALL the focus was on the admittedly robust OUTPUT data, we note the less-focused-upon "Special Question" segment of the survey, which asked:

If you experienced a decline in Production during the 2001 Recession (72.5% of all, did), has Production returned to pre-2001 levels?85.7% replied NO.

Then, If not (85.7% of the 72.5%), WHEN do you expect Production to return to pre-2001 levels?53.1% said between 2Q-4Q 2004 ... BUT the rest, over 43%, said "Not in the Foreseeable Future".

"Indeed, nearly a THIRD of ALL firms stated that Production is NOT likely to regain pre-2001 levels. YET, money supply [growth] is trending well BELOW the degree of stimulus that was on the offer, since pre-2001.

"FAR WORSE, in the macro-secular sense, is this final tidbit from the 'Special Question' segment of the Philly Fed:

"23.4% of the 85.7% of ALL firms that originally stated that Production had not reached back to pre-recession levels, said they did NOT expect Production to reach back to pre-2001 levels ...BECASUSE of ... "Long-term Decline in the Industry."

"Indeed, note the Fed's own text ... 'Moreover, a large percentage of firms (44 percent) do not expect production to return to those pre-recession levels in the foreseeable future, for reasons involving competitiveness or longterm declines in their industries.'"

"YEAH, [he writes sarcastically] lets TRIPLE the Fed Funds rate!!!"

The headlines you read talk about how jobs are getting better. If you look at initial claims, you might get that idea. They are below the psychologically important 400,000 and are dropping ever so slowly. Comparing the real numbers with last year, there is a slight improvement, which is good.

But Continuing Claims are rising, and back to levels seen earlier this year. Taken together, this means that fewer people are losing their jobs, but fewer are also finding jobs.

Let's reflect upon that for a moment. We are told the economy grew by something like 6% in the third quarter. That means with inflation we are talking a nominal rate of over 7% and maybe 8%. That is as powerful as it has been for a long time.

And yet, no jobs. No income growth. As Weldon notes elsewhere, only 2% of those firms surveyed said they were paying lower prices, with 25% paying higher prices, yet 72% say they have no pricing power and are unable to raise prices.

Let's look at where the out-sized growth came from last quarter. Stephen Roach tells us 2% of real GDP growth came from automobile sales in the last two quarters. Consumers, supplied with a tax cut and massive home equity financing from the second quarter as rates briefly dropped to historical lows, took the heavy incentive deals they were offered on cars which were also priced lower than this time last year.

"Surging expenditures on consumer durables [mostly automobiles] accounted for about 2.0 percentage points of annualized real GDP growth, alone, over the past two quarters. To the extent that such an impetus did not reflect the fundamentals of pent-up demand, a payback of like magnitude would not be surprising. Historical experience does, in fact, tell us that's the norm after any spike in durables spending -- let alone the excessive one of the past two quarters. Since 1960, there have been 16 instances of excessive growth in durable goods consumption (defined as an annualized growth contribution exceeding 1.5 percentage points of real GDP) that contributed, on average, 2.2 percentage points of annualized real GDP growth; in the two quarters that followed, the growth contribution slowed dramatically, on average, to just 0.1 percentage point. To the extent such a payback is likely after the current spending burst, it could act as a sharp depressant on overall demand growth in subsequent quarters. That development, in the context of a lingering jobless recovery, could raise serious questions about the staying power of America's current cyclical resurgence." (Stephen Roach of Morgan Stanley)

Could auto sales maintain this level for one more quarter? Perhaps, as small business people all over America come to the end of the year and realize that under the current tax code, if they buy an SUV which weighs over 6,000 pounds (Lincoln Navigator, Cadillac Escalade, Lexus, Chevrolet, Ford, etc,) they may be able to deduct the entire cost from their 2003 taxes. In essence, the government just made these monsters more affordable than smaller cars at two-thirds the price.

(Yes, to my shocked readers in Europe, a 1986 tax rule provides that small businesses can deduct the cost of commercial vehicles, which are defined as small trucks which weigh over 6,000 pounds, which in the US includes large SUVs. The Bush tax stimulus package allows small businesses to deduct up to $100,000 of capital business expenditures immediately per year, up from $25,000 if I remember right. The idea was to get businesses to buy more computers and equipment and furniture, etc. Under the current rules, SUVs also fit into this category. Only in America.)

The good news is that the US economy apparently grew 6% in the third quarter of this year, and should do well this quarter and into the New Year. But this is a stimulus led recovery, and where will the next shove come from? The Bush administration has to hope that oil will drop to around $20, or that rates will somehow come back down.

Roach says, and I agree, "Eager to jump-start the US economy prior to the upcoming presidential election, the Bush Administration focused on front-loaded tax cuts that were designed to have maximum impact in 2004. "Spring-loaded" was the term used by Treasury Secretary John Snow to describe the growth potential of these measures. Well, the White House may have gotten more than it bargained for. The risk, in my view, is that the policy induced stimulus occurred sooner than expected in 2003 -- leaving the US economy having to face the "air-pocket" of a payback in early 2004. Needless to say, that would come during a period of maximum vulnerability insofar as the election cycle is concerned."

---- continua

2 parte

Let's be very clear. There are some very positive signs in the economy. Revenue growth seems to be picking up. There are some anecdotal signs that employment might be starting to rise, although it has not shown up as yet in the data. Housing is still relatively strong, and consumer spending is growing.

Further, I am not complaining about the stimulus driven recovery. Recovery is a good thing. If any of the Democratic presidential hopefuls were currently president and actually pursued the policies they espouse, we really would be experiencing the worst economy since the Hoover administration. Without the combined and powerful stimulus of the Bush tax cuts, federal deficits and Fed engineered lower rates, it is difficult to imagine anything but a severe post bubble and post 9/11 recession.

(The best thing the Republicans have going for them is Howard Dean, who increasingly reminds me of Michael Dukakis, another very liberal Northeastern state governor who came from nowhere to win the Democratic nomination only to go down in flames in the general election. This country might be ready by election time for another centrist Democrat like Lieberman, but a far left Democrat, which Dean clearly is, is not in the cards.)

The point that I am trying to make with the litany of data I provided is that this economy cannot withstand higher interest rates. Do you think home sales, mortgage refinancing and consumer spending, not to mention auto financing and other debt-driven consumption, is ready for higher rates?

This economy is vulnerable in a way that no 6% growth economy in my memory has ever been. If the Fed actually raised interest rates by 1.75% within the next 14 months, pushing mortgages close to 8%, increasing financing costs, impacting home sales and home values, how long would it be before we were staring at a recession and another serious stock market correction?

Further, interest rate increases are dis-inflationary at best, and in this environment, could actually foster deflation. Go back to Parry's statement above, and compare it with scores of other recent Fed speeches and releases. They are worried about the "surprise" of deflation. They see the softness and vulnerability. This is not a Fed that will raise rates until reflation in incomes, pricing power and business investment has demonstrated an ability to sustain themselves in spite of rate increases.

Contradictions: The Fed vs. the Bond Market

Yet, the bond market is pricing in such rates. What are these guys reading (or smoking)? Are you and I, dear reader, the only ones who can understand the clear language of the Fed? Or are we gullible little fish who cannot see through the lies?

And now we come to Bianco's insight. He points to Fannie Mae and Freddie Mac as the culprits for the contradiction between Fed talk and market rates.

Ginnie Mae (the Government National Mortgage Association) is totally owned by the US government and run by the Department of Housing and Urban Development (HUD). Its debt is truly government guaranteed.

Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Association) are private companies. Their debt is not explicitly guaranteed by the government. They do have a $2 billion line of credit with the Treasury which they could use in a liquidity crisis.

But the market treats their debt as if it is guaranteed by the US government. That means Fannie and Freddie can borrow money at much lower rates than can, say, J.P. Morgan or Citibank. I suppose you can argue that is a benefit to consumers, as it does mean that home mortgage rates can be lower as well.

But what Fannie and Freddie have become are Government Sponsored Hedge Funds. Management has taken advantage of their "special" relationship and uses it to increase private profits for shareholders and large salaries, options and bonuses for management.

Essentially, they lend long and borrow short. Since short term rates are lower than long term rates, they pocket the difference. They increase their profits by the use of very large amounts of leverage.

This is known as a "carry trade," and is a regular practice of hedge funds and other investment companies. There is nothing wrong with this. Some of my favorite funds practice this type of investing. Properly practiced, it can produce some steady, if not spectacular, profits.

What Fannie and Freddie do is what good hedge funds should do. They go into the futures market to hedge their interest rate directional risk. You see, if short term rates were to rise above the average rates they have lent to their long term mortgage buyers, they could find themselves in the position of losing money. Lots of money. So they hedge.

They do this in the Eurodollar futures markets. They use swaps or options on swaps called swaptions. (Swaptions are options contracts which, in return for a one-off premium payment, give you the right to enter into a swap agreement at the option expiration.) Again, nothing wrong with this.

Bianco notes the problem lies in that they need over a Trillion Dollars (that's with a "T") of these derivatives. In order to get a trillion dollars to line up on the other side of the trade (to take the risk from Fannie and Freddie), they have to pay a premium. Apparently it may be a big premium.

Bianco argued at lunch, in the shadow of the Chicago futures markets, that it is not the expectations of bond traders for actual rate increases, but the massive need for Fannie and Freddie to hedge its portfolio that drives the Eurodollar rates.

Why do Fannie and Freddie need such high-powered hedge exposure? Because if they acted like Ginnie Mae, their profits would be much less, stock price growth would be lower and management would not get the fancy pay packages and option incentives.

Do I think Fannie and Freddie are at risk today because of this? No, I am not saying that, and neither is Bianco. But there is a limit.

Frank Raines wants to grow his firm (Fannie) 15-20% a year. Where are they going to find more credit worthy risk takers/speculators on the other side of the swaps trade?

Let's be very clear. They could not do this if the market did not price their debt as if it were backed by the US government. The "spread" would not be there. Otherwise, Citigroup and Morgan and other investment banks would be significant competitors.

As long as the market sees that level of risk, the game can continue. But what if they simply try to get too big? How long can you grow a finite market 20% compound a year? What if there is a hiccup? How quickly would the risk premium for the Eurodollar rise? Not very long. The technical term is a "jiffy," which is the name of an actual unit of time which is 1/100 of a second. (The things you learn as you read. Thanks, Art.)

First, if there were a problem, the US Treasury would step in within the next jiffy to provide whatever cash was needed. No administration, Democrat or Republican, will let the US mortgage market and home values crash due to a "liquidity event" at Fannie or Freddie. Think the Savings and Loan crisis was big? It would be a picnic compared to a major problem with Fannie and Freddie. The implicit guarantee the markets perceive is actually quite real. These firms are too big and too important to fail. The ultimate insurance tab, however, is picked up by the US taxpayer.

For every $100 billion their "hedge book" increases, the costs for acquiring the hedge is evidently rising. What is the point when we get to "too much?" I don't know, and neither does anyone else. We may be a long way from there, or maybe not.

The point is that a private company seeking private gains should not be putting the entire US mortgage market and the US taxpayer at risk, even if they think the risk is small.

The management of these firms is comprised of very smart men and women, and I am sure they employ some of the smartest PhDs anywhere to run their hedge book. But so did Long Term Capital Management.

Where's the Market Discipline?

The problem with Long Term Capital Management (LTCM) was that there were no market restraints or market discipline on the firm. Greed drove all those investment banks to lend LTCM money in the lust for commissions, and LTCM refused to show any of the firms their "hedge book." You can bet if the investment banks had seen their total exposure, they would have reined the Nobel Prize management team in, in very short order.

But who is looking over Fannie's shoulder? "Don't micro-manage us," say Raines. Translation: don't mess up our gravy train.

Everyone seems to acknowledge that federal oversight is weak. There is now a bill in Congress to move the oversight to the Treasury Department, but Fannie and Freddie lobbyists have so watered down the bill that it is worse than the current situation. If oversight goes to the Treasury under the current guidelines, that increases the implicit government guarantee and US taxpayer exposure. But if creates no real controls.

If Fannie and Freddie want the advantage of an all but explicit government guarantee, they should open their hedge book to complete scrutiny and be subject to leverage curbs. At a minimum, they should be made to shorten their duration risk exposure (another risk which I will not take the space to go into, but which is real enough).

Yes, under such a situation they will not make as much profit as they do today. But so what? Why should a small group place the rest of us with a large risk, even if it is thought to be remote?

We would scream if a Morgan or a Citigroup or some other private firm would be allowed to put US taxpayers at risk for private gain. What is the difference with Fannie or Freddie?

Alan Greenspan argues, and I think rightly, that the Fed should manage not for the more likely of problems, but for the possible problems which would cause the most harm. It is better to tolerate some problems than to experience a problem which could lead to disaster.

The mortgage debt market is now larger than the government debt market. One can make an argument it is the most significant piece of the US economy. Why take any risk at all?

Yet, if Bianco is right, the bond market sees more than a little risk, and that is why interest rate futures are priced so high in the face of the Fed telling us rates are going nowhere. If there were no risk to this trade, there would not be such high risk premiums.

Congress needs to shorten the leash on Fannie and Freddie. Public or private. In or out. But not both. Perhaps Fannie and Freddie are right. Maybe the risk is low. But so was the risk to Long Term Capital. It is a risk that US tax-payers should not take, are not paid to take, yet Congress has let the lobbyists convince them otherwise.

More Contradictions.

How can we once again be in Bubble valuations? Amazon at a P/E 0f 151, Priceline at 220 and the list goes on and on. Caroline Baum points out the China has lost 10,000,000 manufacturing jobs in the last few years due to productivity increases. Who do the Chinese politicians blame? Who is their currency scapegoat? Our politicians on both sides of the aisle pander to our nationalistic tendencies, as do politicians world-wide. Do we really want China to risk major turmoil and a reactionary return to a nationalistic world. Think Germany in 1932.

What of the clear contradiction between the argument for free trade and the seeming arrival of protectionist sentiment upon every shore throughout the world?

Enough. There are just too many, and it is time to go home.

Let me suggest that the hedge funds and major traders who read me might go to Greg Weldon's web site mentioned above and contact him directly. He has a rather pricey (several thousand a year) service in addition to his less expensive retail letters. I am sure he will send you a few weeks' samples. They are worth every penny if you are "working the markets."

If you would like to meet in New Orleans October 29-31, please let my office know. If you have already written about getting together, you should have been contacted by now. Have yourself a great week.

Your almost ready to finish his book analyst,

John Mauldin

johnmauldin@investorsinsight.com

Copyright 2003 John Mauldin. All Rights Reserved

If you would like to reproduce any of John Mauldin's E-Letters you must include the source of your quote and an email address (johnmauldi@investorsinsight.com) Please write to reproductions@investorsinsight.com and inform us of any reproductions. Please include where and when the copy will be reproduced.

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above.

-- Posted Sunday, October 19 2003

bye

Let's be very clear. There are some very positive signs in the economy. Revenue growth seems to be picking up. There are some anecdotal signs that employment might be starting to rise, although it has not shown up as yet in the data. Housing is still relatively strong, and consumer spending is growing.

Further, I am not complaining about the stimulus driven recovery. Recovery is a good thing. If any of the Democratic presidential hopefuls were currently president and actually pursued the policies they espouse, we really would be experiencing the worst economy since the Hoover administration. Without the combined and powerful stimulus of the Bush tax cuts, federal deficits and Fed engineered lower rates, it is difficult to imagine anything but a severe post bubble and post 9/11 recession.

(The best thing the Republicans have going for them is Howard Dean, who increasingly reminds me of Michael Dukakis, another very liberal Northeastern state governor who came from nowhere to win the Democratic nomination only to go down in flames in the general election. This country might be ready by election time for another centrist Democrat like Lieberman, but a far left Democrat, which Dean clearly is, is not in the cards.)

The point that I am trying to make with the litany of data I provided is that this economy cannot withstand higher interest rates. Do you think home sales, mortgage refinancing and consumer spending, not to mention auto financing and other debt-driven consumption, is ready for higher rates?

This economy is vulnerable in a way that no 6% growth economy in my memory has ever been. If the Fed actually raised interest rates by 1.75% within the next 14 months, pushing mortgages close to 8%, increasing financing costs, impacting home sales and home values, how long would it be before we were staring at a recession and another serious stock market correction?

Further, interest rate increases are dis-inflationary at best, and in this environment, could actually foster deflation. Go back to Parry's statement above, and compare it with scores of other recent Fed speeches and releases. They are worried about the "surprise" of deflation. They see the softness and vulnerability. This is not a Fed that will raise rates until reflation in incomes, pricing power and business investment has demonstrated an ability to sustain themselves in spite of rate increases.

Contradictions: The Fed vs. the Bond Market

Yet, the bond market is pricing in such rates. What are these guys reading (or smoking)? Are you and I, dear reader, the only ones who can understand the clear language of the Fed? Or are we gullible little fish who cannot see through the lies?

And now we come to Bianco's insight. He points to Fannie Mae and Freddie Mac as the culprits for the contradiction between Fed talk and market rates.

Ginnie Mae (the Government National Mortgage Association) is totally owned by the US government and run by the Department of Housing and Urban Development (HUD). Its debt is truly government guaranteed.

Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Association) are private companies. Their debt is not explicitly guaranteed by the government. They do have a $2 billion line of credit with the Treasury which they could use in a liquidity crisis.

But the market treats their debt as if it is guaranteed by the US government. That means Fannie and Freddie can borrow money at much lower rates than can, say, J.P. Morgan or Citibank. I suppose you can argue that is a benefit to consumers, as it does mean that home mortgage rates can be lower as well.

But what Fannie and Freddie have become are Government Sponsored Hedge Funds. Management has taken advantage of their "special" relationship and uses it to increase private profits for shareholders and large salaries, options and bonuses for management.

Essentially, they lend long and borrow short. Since short term rates are lower than long term rates, they pocket the difference. They increase their profits by the use of very large amounts of leverage.

This is known as a "carry trade," and is a regular practice of hedge funds and other investment companies. There is nothing wrong with this. Some of my favorite funds practice this type of investing. Properly practiced, it can produce some steady, if not spectacular, profits.

What Fannie and Freddie do is what good hedge funds should do. They go into the futures market to hedge their interest rate directional risk. You see, if short term rates were to rise above the average rates they have lent to their long term mortgage buyers, they could find themselves in the position of losing money. Lots of money. So they hedge.

They do this in the Eurodollar futures markets. They use swaps or options on swaps called swaptions. (Swaptions are options contracts which, in return for a one-off premium payment, give you the right to enter into a swap agreement at the option expiration.) Again, nothing wrong with this.

Bianco notes the problem lies in that they need over a Trillion Dollars (that's with a "T") of these derivatives. In order to get a trillion dollars to line up on the other side of the trade (to take the risk from Fannie and Freddie), they have to pay a premium. Apparently it may be a big premium.

Bianco argued at lunch, in the shadow of the Chicago futures markets, that it is not the expectations of bond traders for actual rate increases, but the massive need for Fannie and Freddie to hedge its portfolio that drives the Eurodollar rates.

Why do Fannie and Freddie need such high-powered hedge exposure? Because if they acted like Ginnie Mae, their profits would be much less, stock price growth would be lower and management would not get the fancy pay packages and option incentives.

Do I think Fannie and Freddie are at risk today because of this? No, I am not saying that, and neither is Bianco. But there is a limit.

Frank Raines wants to grow his firm (Fannie) 15-20% a year. Where are they going to find more credit worthy risk takers/speculators on the other side of the swaps trade?

Let's be very clear. They could not do this if the market did not price their debt as if it were backed by the US government. The "spread" would not be there. Otherwise, Citigroup and Morgan and other investment banks would be significant competitors.

As long as the market sees that level of risk, the game can continue. But what if they simply try to get too big? How long can you grow a finite market 20% compound a year? What if there is a hiccup? How quickly would the risk premium for the Eurodollar rise? Not very long. The technical term is a "jiffy," which is the name of an actual unit of time which is 1/100 of a second. (The things you learn as you read. Thanks, Art.)

First, if there were a problem, the US Treasury would step in within the next jiffy to provide whatever cash was needed. No administration, Democrat or Republican, will let the US mortgage market and home values crash due to a "liquidity event" at Fannie or Freddie. Think the Savings and Loan crisis was big? It would be a picnic compared to a major problem with Fannie and Freddie. The implicit guarantee the markets perceive is actually quite real. These firms are too big and too important to fail. The ultimate insurance tab, however, is picked up by the US taxpayer.

For every $100 billion their "hedge book" increases, the costs for acquiring the hedge is evidently rising. What is the point when we get to "too much?" I don't know, and neither does anyone else. We may be a long way from there, or maybe not.

The point is that a private company seeking private gains should not be putting the entire US mortgage market and the US taxpayer at risk, even if they think the risk is small.

The management of these firms is comprised of very smart men and women, and I am sure they employ some of the smartest PhDs anywhere to run their hedge book. But so did Long Term Capital Management.

Where's the Market Discipline?

The problem with Long Term Capital Management (LTCM) was that there were no market restraints or market discipline on the firm. Greed drove all those investment banks to lend LTCM money in the lust for commissions, and LTCM refused to show any of the firms their "hedge book." You can bet if the investment banks had seen their total exposure, they would have reined the Nobel Prize management team in, in very short order.

But who is looking over Fannie's shoulder? "Don't micro-manage us," say Raines. Translation: don't mess up our gravy train.

Everyone seems to acknowledge that federal oversight is weak. There is now a bill in Congress to move the oversight to the Treasury Department, but Fannie and Freddie lobbyists have so watered down the bill that it is worse than the current situation. If oversight goes to the Treasury under the current guidelines, that increases the implicit government guarantee and US taxpayer exposure. But if creates no real controls.

If Fannie and Freddie want the advantage of an all but explicit government guarantee, they should open their hedge book to complete scrutiny and be subject to leverage curbs. At a minimum, they should be made to shorten their duration risk exposure (another risk which I will not take the space to go into, but which is real enough).

Yes, under such a situation they will not make as much profit as they do today. But so what? Why should a small group place the rest of us with a large risk, even if it is thought to be remote?

We would scream if a Morgan or a Citigroup or some other private firm would be allowed to put US taxpayers at risk for private gain. What is the difference with Fannie or Freddie?

Alan Greenspan argues, and I think rightly, that the Fed should manage not for the more likely of problems, but for the possible problems which would cause the most harm. It is better to tolerate some problems than to experience a problem which could lead to disaster.

The mortgage debt market is now larger than the government debt market. One can make an argument it is the most significant piece of the US economy. Why take any risk at all?

Yet, if Bianco is right, the bond market sees more than a little risk, and that is why interest rate futures are priced so high in the face of the Fed telling us rates are going nowhere. If there were no risk to this trade, there would not be such high risk premiums.

Congress needs to shorten the leash on Fannie and Freddie. Public or private. In or out. But not both. Perhaps Fannie and Freddie are right. Maybe the risk is low. But so was the risk to Long Term Capital. It is a risk that US tax-payers should not take, are not paid to take, yet Congress has let the lobbyists convince them otherwise.

More Contradictions.

How can we once again be in Bubble valuations? Amazon at a P/E 0f 151, Priceline at 220 and the list goes on and on. Caroline Baum points out the China has lost 10,000,000 manufacturing jobs in the last few years due to productivity increases. Who do the Chinese politicians blame? Who is their currency scapegoat? Our politicians on both sides of the aisle pander to our nationalistic tendencies, as do politicians world-wide. Do we really want China to risk major turmoil and a reactionary return to a nationalistic world. Think Germany in 1932.

What of the clear contradiction between the argument for free trade and the seeming arrival of protectionist sentiment upon every shore throughout the world?

Enough. There are just too many, and it is time to go home.

Let me suggest that the hedge funds and major traders who read me might go to Greg Weldon's web site mentioned above and contact him directly. He has a rather pricey (several thousand a year) service in addition to his less expensive retail letters. I am sure he will send you a few weeks' samples. They are worth every penny if you are "working the markets."

If you would like to meet in New Orleans October 29-31, please let my office know. If you have already written about getting together, you should have been contacted by now. Have yourself a great week.

Your almost ready to finish his book analyst,

John Mauldin

johnmauldin@investorsinsight.com

Copyright 2003 John Mauldin. All Rights Reserved

If you would like to reproduce any of John Mauldin's E-Letters you must include the source of your quote and an email address (johnmauldi@investorsinsight.com) Please write to reproductions@investorsinsight.com and inform us of any reproductions. Please include where and when the copy will be reproduced.

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above.

-- Posted Sunday, October 19 2003

bye

Movimenti sui tassi

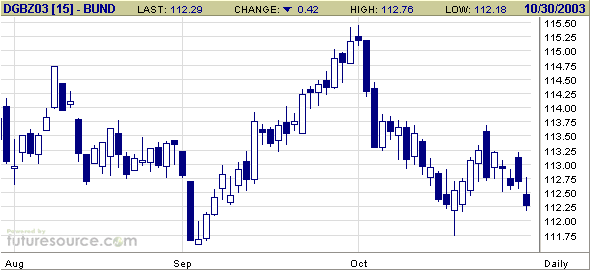

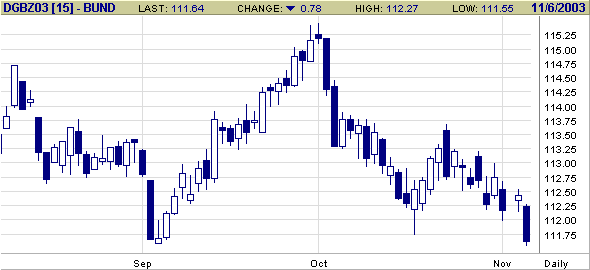

14:50 Futures Bund dicembre segna minimo contratto su dati Usa sussidi

LONDRA, 6 novembre (Reuters) - Il futures Bund a dicembre ha segnato un nuovo minimo del contratto a 111,55 dopo i dati sui nuovi disoccupati settimanali negli Stati Uniti, scesi al minimo da gennaio 2001.

Il dato settimanale sulle richieste di sussidio precede di solo un giorno le statistiche sulla disoccupazione negli Usa in ottobre, su cui è puntata da giorni l'attenzione del mercato.

Sulla scia delle cifre Usa ha accentuato pesantemente la flessione anche la scadenza marzo dei futures Euribor, che è arrivato a 97,615 prima di rimbalzare a 97,635 (-0,035).

Alle 14,50 il futures Bund a dicembre cede 71 centesimi a 111,71.

----------------------------------------------------------------------------

09:19 Bond euro, futures Bund scivola a minimo tre settimane

6 novembre (Reuters) * Apertura in deciso ribasso per i governativi europei poche ore prima dell'annuncio delle decisioni sui tassi della Banca centrale europea e di Banca d'Inghilterra

* Il futures a dicembre sul Bund è scivolato fino a 111,76, minimo dal 17 ottobre, dopo la rottura di un supporto posizionato a 112 sui grafici

* "C'erano alcuni ordini stop-loss attorno a 112 e ora sono stati eliminati, credo che risaliremo", commenta un trader * Le attese sono per un taglio di 25 punti base dei tassi di

riferimento britannici e per una conferma dei tassi eurozona

* I riflettori sono puntati sul neopresidente Bce, Jean-Claude Trichet, che terrà la sua prima conferenza stampa oggi alle 14,30

========================= ORE 09,05 =============

VARIAZIONE RENDIMENTO

FUTURES EURIBOR DIC. 97,800 (-0,01)

FUTURES BUND 112,07 (-0,35)

BUND 10 ANNI 98,70 (-0,32) 4,41%

BUND 30 ANNI 95,58 (-0,54) 5,03%

==============================================

----------------------------------------------------------------------------

14:33 Monetario,futures Euribor marzo accentua calo dopo Bce e BoE

MILANO, 6 novembre (Reuters) - I derivati sui tassi di interesse accentuano la flessione dopo le decisioni sui tassi di Banca d'Inghilterra e della Banca centrale europea, che pure hanno rispettato le attese dei mercati. Come previsto,

Bank of England

ha seguito l'esempio della Reserve Bank of Australia,

alzando di un quarto di punto i tassi di riferimento, ora al 3,75%.

Scontata anche la conferma dei tassi eurozona; i riflettori sono puntati piuttosto sulla prima conferenza stampa del neopresidente Bce Jean-Claude Trichet.

Alle 16,00 italiane, il governatore della Federal Reserve, Alan Greenspan, parlerà della situazione dell'economia Usa, nel suo primo intervento sul tema da luglio scorso. Attesa anche per i dati Usa sul mercato del lavoro, in pubblicazione domani.

Attorno alle 14,30

il futures Euribor a dicembre cede 0,05 a 97,805, invariato da ieri mattina;

la scadenza marzo 2004 scende di 0,035 a 97,655, da 97,640 mercoledì alla stessa ora.

Leggera correzione a rialzo sulle scadenze medio-lunghe della curva Eonia swap: l'anno passa a 2,38/40% da 2,34/36%. I tre mesi sono stabili a 2,08/10%, i sei salgono a 2,15/17 da a

2,13/15%.

Invariata, come negli ultimi giorni, la situazione sul mercato dei depositi interbancari: overnight piatto a 2,04%, tom/next e spot/next allineati a 2,04/05%.

bye

14:50 Futures Bund dicembre segna minimo contratto su dati Usa sussidi

LONDRA, 6 novembre (Reuters) - Il futures Bund a dicembre ha segnato un nuovo minimo del contratto a 111,55 dopo i dati sui nuovi disoccupati settimanali negli Stati Uniti, scesi al minimo da gennaio 2001.

Il dato settimanale sulle richieste di sussidio precede di solo un giorno le statistiche sulla disoccupazione negli Usa in ottobre, su cui è puntata da giorni l'attenzione del mercato.

Sulla scia delle cifre Usa ha accentuato pesantemente la flessione anche la scadenza marzo dei futures Euribor, che è arrivato a 97,615 prima di rimbalzare a 97,635 (-0,035).

Alle 14,50 il futures Bund a dicembre cede 71 centesimi a 111,71.

----------------------------------------------------------------------------

09:19 Bond euro, futures Bund scivola a minimo tre settimane

6 novembre (Reuters) * Apertura in deciso ribasso per i governativi europei poche ore prima dell'annuncio delle decisioni sui tassi della Banca centrale europea e di Banca d'Inghilterra

* Il futures a dicembre sul Bund è scivolato fino a 111,76, minimo dal 17 ottobre, dopo la rottura di un supporto posizionato a 112 sui grafici

* "C'erano alcuni ordini stop-loss attorno a 112 e ora sono stati eliminati, credo che risaliremo", commenta un trader * Le attese sono per un taglio di 25 punti base dei tassi di

riferimento britannici e per una conferma dei tassi eurozona

* I riflettori sono puntati sul neopresidente Bce, Jean-Claude Trichet, che terrà la sua prima conferenza stampa oggi alle 14,30

========================= ORE 09,05 =============

VARIAZIONE RENDIMENTO

FUTURES EURIBOR DIC. 97,800 (-0,01)

FUTURES BUND 112,07 (-0,35)

BUND 10 ANNI 98,70 (-0,32) 4,41%

BUND 30 ANNI 95,58 (-0,54) 5,03%

==============================================

----------------------------------------------------------------------------

14:33 Monetario,futures Euribor marzo accentua calo dopo Bce e BoE

MILANO, 6 novembre (Reuters) - I derivati sui tassi di interesse accentuano la flessione dopo le decisioni sui tassi di Banca d'Inghilterra e della Banca centrale europea, che pure hanno rispettato le attese dei mercati. Come previsto,

Bank of England

ha seguito l'esempio della Reserve Bank of Australia,

alzando di un quarto di punto i tassi di riferimento, ora al 3,75%.

Scontata anche la conferma dei tassi eurozona; i riflettori sono puntati piuttosto sulla prima conferenza stampa del neopresidente Bce Jean-Claude Trichet.

Alle 16,00 italiane, il governatore della Federal Reserve, Alan Greenspan, parlerà della situazione dell'economia Usa, nel suo primo intervento sul tema da luglio scorso. Attesa anche per i dati Usa sul mercato del lavoro, in pubblicazione domani.

Attorno alle 14,30

il futures Euribor a dicembre cede 0,05 a 97,805, invariato da ieri mattina;

la scadenza marzo 2004 scende di 0,035 a 97,655, da 97,640 mercoledì alla stessa ora.

Leggera correzione a rialzo sulle scadenze medio-lunghe della curva Eonia swap: l'anno passa a 2,38/40% da 2,34/36%. I tre mesi sono stabili a 2,08/10%, i sei salgono a 2,15/17 da a

2,13/15%.

Invariata, come negli ultimi giorni, la situazione sul mercato dei depositi interbancari: overnight piatto a 2,04%, tom/next e spot/next allineati a 2,04/05%.

bye

ASTE META' MESE

18:09 Tesoro riapre Btp 3, 5, 15 anni in asta 13 novembre

ROMA, 6 novembre (Reuters) - Il ministero dell'Economia e

delle finanze ha disposto che in occasione dell'asta del 13

novembre di titoli a medio lungo saranno posti in vendita i

seguenti titoli:

* undicesima tranche BTP 01-09-06, cedola 2,75%

* quinta tranche BTP 15-09-08, cedola 3,50%

* settima tranche Btp 01-02-19, cedola 4,25%

Lo dice un comunicato riportato sulla pagina Reuters

Le quantità saranno comunicate lunedi 10 novembre

Aste * 13 novembre entro le ore 11,00 Regolamento * lunedì 17 novembre

18:04 Tesoro offre 3,25 mld Bot 3 mesi, 4,5 mld Bot 12 mesi

ROMA, 6 novembre (Reuters) - Il ministero dell'Economia e

delle finanze offrirà all'asta dell'11 novembre 7,75 mld di Bot

contro i 7,25 mld in scadenza. Lo si legge sulle pagine Reuters .

* Bot 3 mesi (94 gg) 16-02-04 offerti 3,25 mld

* Bot 12 mesi (367) 15-11-04 offerti 4,5 mld

Le offerte vanno presentate entro le ore 11 dell'11

novembre, regolamento il 14 novembre. A fine ottobre erano in circolazione 137,420 mld di Bot suddivisi in 1 mld a 263 gg., 2 mld a 233 gg., 10,250 mld a tre mesi, 50,670 mld a 6 mesi e 73,5 mld a un anno.

PS La richiesta alla banca un giorno prima

18:09 Tesoro riapre Btp 3, 5, 15 anni in asta 13 novembre

ROMA, 6 novembre (Reuters) - Il ministero dell'Economia e

delle finanze ha disposto che in occasione dell'asta del 13

novembre di titoli a medio lungo saranno posti in vendita i

seguenti titoli:

* undicesima tranche BTP 01-09-06, cedola 2,75%

* quinta tranche BTP 15-09-08, cedola 3,50%

* settima tranche Btp 01-02-19, cedola 4,25%

Lo dice un comunicato riportato sulla pagina Reuters

Le quantità saranno comunicate lunedi 10 novembre

Aste * 13 novembre entro le ore 11,00 Regolamento * lunedì 17 novembre

18:04 Tesoro offre 3,25 mld Bot 3 mesi, 4,5 mld Bot 12 mesi

ROMA, 6 novembre (Reuters) - Il ministero dell'Economia e

delle finanze offrirà all'asta dell'11 novembre 7,75 mld di Bot

contro i 7,25 mld in scadenza. Lo si legge sulle pagine Reuters .

* Bot 3 mesi (94 gg) 16-02-04 offerti 3,25 mld

* Bot 12 mesi (367) 15-11-04 offerti 4,5 mld

Le offerte vanno presentate entro le ore 11 dell'11

novembre, regolamento il 14 novembre. A fine ottobre erano in circolazione 137,420 mld di Bot suddivisi in 1 mld a 263 gg., 2 mld a 233 gg., 10,250 mld a tre mesi, 50,670 mld a 6 mesi e 73,5 mld a un anno.

PS La richiesta alla banca un giorno prima

Aste di oggi - risultati

11:21 Asta Bot 12 mesi, rendimento lordo in rialzo a 2,369% da 2,187%

MILANO, 11 novembre (Reuters) - Bankitalia rende noti i seguenti risultati dell'asta tenutasi oggi sul

Bot 15 novembre 2004.

Assegnati: 4,5 mld Chiesti: 15,833 mld

................. Asta 11/11 ....... Asta 10/10

Durata 367 gg 366 gg

Prezzo medio 97,641 97,825

Rendimento lordo 2,369% 2,187%

Riparto 54,661

Prezzo fiscale 97,641

Codice 356146

Regolamento 14/11/2003

11:20 Asta Bot 3 mesi, rendimento lordo a 2,006% da 1,998%

MILANO, 11 novembre (Reuters) - Bankitalia rende noti i seguenti risultati dell'asta tenutasi oggi sul

Bot 16 febbraio 2004.

Assegnati: 3,25 mld Chiesti: 8,232 mld

................. Asta 11/11 ........ Asta 10/10

Durata 94 gg 92 gg

Prezzo medio 99,479 99,492

Rendimento lordo 2,006% 1,998%

Riparto 10,676

Prezzo fiscale 99,479

Codice 356145

Regolamento 14/11/2003

bye

11:21 Asta Bot 12 mesi, rendimento lordo in rialzo a 2,369% da 2,187%

MILANO, 11 novembre (Reuters) - Bankitalia rende noti i seguenti risultati dell'asta tenutasi oggi sul

Bot 15 novembre 2004.

Assegnati: 4,5 mld Chiesti: 15,833 mld

................. Asta 11/11 ....... Asta 10/10

Durata 367 gg 366 gg

Prezzo medio 97,641 97,825

Rendimento lordo 2,369% 2,187%

Riparto 54,661

Prezzo fiscale 97,641

Codice 356146

Regolamento 14/11/2003

11:20 Asta Bot 3 mesi, rendimento lordo a 2,006% da 1,998%

MILANO, 11 novembre (Reuters) - Bankitalia rende noti i seguenti risultati dell'asta tenutasi oggi sul

Bot 16 febbraio 2004.

Assegnati: 3,25 mld Chiesti: 8,232 mld

................. Asta 11/11 ........ Asta 10/10

Durata 94 gg 92 gg

Prezzo medio 99,479 99,492

Rendimento lordo 2,006% 1,998%

Riparto 10,676

Prezzo fiscale 99,479

Codice 356145

Regolamento 14/11/2003

bye

Economia, martedì 11 novembre 2003 - 17:26

BCE: ISSING SEGNALA FINE CICLO ALLENTAMENTO MONETARIO

(ANSA) - FRANCOFORTE, 11 NOV - Il capoeconomista della Bce,

Otmar Issing, ha lasciato intendere oggi che la Bce ha ormai

concluso il suo ciclo di allentamento monetario. In

un'intervista rilasciata a Afx, Issing ha dichiarato infatti che

''non c'e' piu' niente che la Bce possa fare'' per gettare le

fondamenta della ripresa economica. L'economista ha manifestato, tuttavia, qualche preoccupazione sul potenziale di crescita nel medio termine di Eurolandia, sottolineando che le continue violazioni del Patto di stabilita' stanno minando la fiducia, che rappresenta uno degli elementi chiave della crescita

economica. (ANSA)

Economia, martedì 11 novembre 2003 - 18:48

BCE: ISSING SEGNALA FINE CICLO ALLENTAMENTO MONETARIO (2)

(ANSA) - FRANCOFORTE, 11 NOV - "Il Patto è un elemento istituzionale importante dell´unione monetaria. Metterlo in dubbio mina la fiducia. E´ questa la nostra preoccupazione principale", ha proseguito Issing, ribadendo come, sotto il profilo della politica monetaria, "abbiamo avuto tassi di interesse molto bassi per un periodo di tempo abbondante. Il terreno è preparato, per cui non c´é niente di più che la politica monetaria possa fare". Dal punto di vista macroeconomico, Issing ha sottolineato che"la nostra fiducia nella ripresa è gradualmente aumentata negli ultimi mesi. Siamo più fiduciosi di quanto lo fossimo, diciamo, tre mesi fa". Riguardo al potenziale di crescita, infine, il banchiere centrale ha spiegato che Eurolandia lo raggiungerà "nella seconda metà dell´anno prossimo", rilevando tuttavia che un potenziale del 2,5% non è sufficientee che occorre aumentarlo, considerando i molti problemi che sitrova ad affrontare l´Europa. (ANSA)

bye

BCE: ISSING SEGNALA FINE CICLO ALLENTAMENTO MONETARIO

(ANSA) - FRANCOFORTE, 11 NOV - Il capoeconomista della Bce,

Otmar Issing, ha lasciato intendere oggi che la Bce ha ormai

concluso il suo ciclo di allentamento monetario. In

un'intervista rilasciata a Afx, Issing ha dichiarato infatti che

''non c'e' piu' niente che la Bce possa fare'' per gettare le

fondamenta della ripresa economica. L'economista ha manifestato, tuttavia, qualche preoccupazione sul potenziale di crescita nel medio termine di Eurolandia, sottolineando che le continue violazioni del Patto di stabilita' stanno minando la fiducia, che rappresenta uno degli elementi chiave della crescita

economica. (ANSA)

Economia, martedì 11 novembre 2003 - 18:48

BCE: ISSING SEGNALA FINE CICLO ALLENTAMENTO MONETARIO (2)

(ANSA) - FRANCOFORTE, 11 NOV - "Il Patto è un elemento istituzionale importante dell´unione monetaria. Metterlo in dubbio mina la fiducia. E´ questa la nostra preoccupazione principale", ha proseguito Issing, ribadendo come, sotto il profilo della politica monetaria, "abbiamo avuto tassi di interesse molto bassi per un periodo di tempo abbondante. Il terreno è preparato, per cui non c´é niente di più che la politica monetaria possa fare". Dal punto di vista macroeconomico, Issing ha sottolineato che"la nostra fiducia nella ripresa è gradualmente aumentata negli ultimi mesi. Siamo più fiduciosi di quanto lo fossimo, diciamo, tre mesi fa". Riguardo al potenziale di crescita, infine, il banchiere centrale ha spiegato che Eurolandia lo raggiungerà "nella seconda metà dell´anno prossimo", rilevando tuttavia che un potenziale del 2,5% non è sufficientee che occorre aumentarlo, considerando i molti problemi che sitrova ad affrontare l´Europa. (ANSA)

bye

ASTE BTP

11:21 Atsa Btp a 15 anni, rendimento lordo sale a 4,89% da 4,78%

MILANO, 13 novembre (Reuters) - Bankitalia comunica i seguenti risultati dell'asta di oggi sulla settima tranche del

Btp primo febbraio 2019, cedola 4,25%.

Importo richiesto: 4,555 mld Importo assegnato: 2,5 mld Codice: 349325

Asta 13/11 Asta 13/10

Prezzo aggiudicazione 93,75 94,80

Prezzo esclusione 91,880 93,093

Rendimento lordo 4,89% 4,78%

Riparto 49,910%

Importo in circolazione (mln) 13.690

Importo assegnato ultime 3 aste (mln) 6.293

Riapertura (mln) 250

Dietimi (gg) 108 gg

Regolamento 17/11/2003

Prezzo nettisti 93,744807

11:21 Asta Btp a tre anni, rendimento sale a 3,11% da 3,02

MILANO, 13 novembre (Reuters) - Bankitalia comunica i seguenti risultati dell'asta odierna sull'undicesima tranche del

Btp primo settembre 2006, cedola 2,75%.

Importo richiesto: 3,533 mld Importo assegnato: 2 mld Codice: 352225

Asta 13/11 Asta 30/10

Prezzo aggiudicazione 99,10 99,33

Prezzo esclusione 97,143 97,383

Rendimento lordo 3,11% 3,02%

Riparto 36,440%

Importo in circolazione (mln) 13.575

Importo assegnato ultime 3 aste (mln) 4.979

Riapertura (mln) 200

Dietimi (gg) 77

Regolamento 17/11/2003

Prezzo nettisti 99,093765

11:20 Asta Btp 15 settembre 2008, rendimento sale a 3,73% da 3,53%

MILANO, 13 novembre (Reuters) - Bankitalia comunica i seguenti risultati dell'asta odierna sulla quinta tranche del

Btp 15 settembre 2008, cedola 3,5%.

Importo richiesto: 3,818 mld Importo assegnato: 2 mld Codice: 353209

Asta 13/11 Asta 13/10

Prezzo aggiudicazione 99,12 99,97

Prezzo esclusione 97,189 98,144

Rendimento lordo 3,73% 3,53%

Riparto 71,665

Importo in circolazione (mln) 7.500

Importo assegnato ultime 3 aste (mln) 6.525

Riapertura (mln) 200

Dietimi (gg) 63

Regolamento 17/11/2003

Prezzo nettisti 99,12

bye

11:21 Atsa Btp a 15 anni, rendimento lordo sale a 4,89% da 4,78%

MILANO, 13 novembre (Reuters) - Bankitalia comunica i seguenti risultati dell'asta di oggi sulla settima tranche del

Btp primo febbraio 2019, cedola 4,25%.

Importo richiesto: 4,555 mld Importo assegnato: 2,5 mld Codice: 349325

Asta 13/11 Asta 13/10

Prezzo aggiudicazione 93,75 94,80

Prezzo esclusione 91,880 93,093

Rendimento lordo 4,89% 4,78%

Riparto 49,910%

Importo in circolazione (mln) 13.690

Importo assegnato ultime 3 aste (mln) 6.293

Riapertura (mln) 250

Dietimi (gg) 108 gg

Regolamento 17/11/2003

Prezzo nettisti 93,744807

11:21 Asta Btp a tre anni, rendimento sale a 3,11% da 3,02

MILANO, 13 novembre (Reuters) - Bankitalia comunica i seguenti risultati dell'asta odierna sull'undicesima tranche del

Btp primo settembre 2006, cedola 2,75%.

Importo richiesto: 3,533 mld Importo assegnato: 2 mld Codice: 352225

Asta 13/11 Asta 30/10

Prezzo aggiudicazione 99,10 99,33

Prezzo esclusione 97,143 97,383

Rendimento lordo 3,11% 3,02%

Riparto 36,440%

Importo in circolazione (mln) 13.575

Importo assegnato ultime 3 aste (mln) 4.979

Riapertura (mln) 200

Dietimi (gg) 77

Regolamento 17/11/2003

Prezzo nettisti 99,093765

11:20 Asta Btp 15 settembre 2008, rendimento sale a 3,73% da 3,53%

MILANO, 13 novembre (Reuters) - Bankitalia comunica i seguenti risultati dell'asta odierna sulla quinta tranche del

Btp 15 settembre 2008, cedola 3,5%.

Importo richiesto: 3,818 mld Importo assegnato: 2 mld Codice: 353209

Asta 13/11 Asta 13/10

Prezzo aggiudicazione 99,12 99,97

Prezzo esclusione 97,189 98,144

Rendimento lordo 3,73% 3,53%

Riparto 71,665